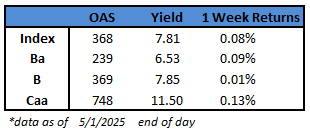

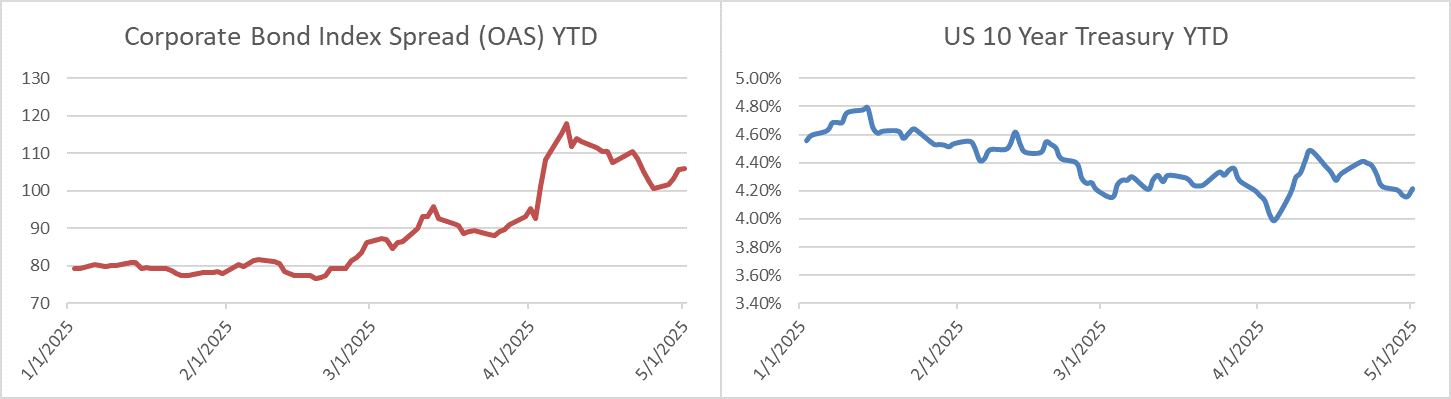

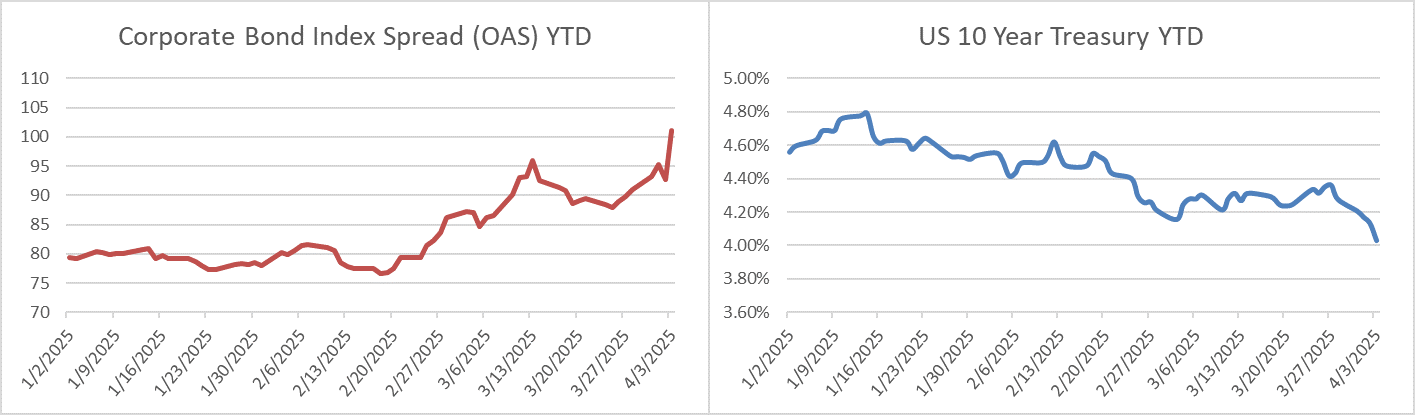

Credit spreads moved materially tighter this week as investors embraced risk across all markets on the back of subsiding fears surrounding some of the worst outcomes for global trade. The US Corporate Bond Index closed last week at 99 and had tightened to 91 as the market closed on Thursday. The 10yr Treasury yield started the week higher on trade enthusiasm and then traded within a narrow range for most of the week. The benchmark rate closed last Friday at 4.38% and it was 4.43% by Thursday’s close. Through Thursday, the Corporate Bond Index year-to-date total return was +1.53% while the yield to maturity for the Index closed the day at 5.30%.

Economics

There was a bounty of economic data this week. The CPI print for the month of April was relatively benign. Core CPI has risen 2.8% over the past year and at an annualized rate of 2.1% over the past three months, which is an improvement relative to the same time period last year. The FOMC is likely pleased with this print but also cognizant of the fact that it does not fully reflect the rapid change in trade policy. Retail sales were slightly better than expectations for the month of April and March data was revised higher but, again, there was much noise in the data due to tariff impacts and it will take some time to see how much spring spending was pulled forward by consumers in order to get ahead of price increases. Both small business and consumer confidence continued to decline, which could impact labor demand and consumer spending in the future. Finally, housing starts posted a nice bump in April but a deeper dive into the data showed a collapse in building permits suggesting weaker activity in the ensuing months.

Next week is a very light calendar of economic data domestically. Globally, both the UK and Japan will release inflation numbers that could give investors an idea of what those central bank’s will be looking to do with their policy rates.

Primary Market

It was a brisk week for issuance as companies priced $40bln in new debt besting projections of $35bln. Concessions were reasonable and investor demand was solid putting the primary market in a “well balanced” state in our view. To expand a bit on our thoughts, we viewed pricing for most issues this week as favorable against a demand backdrop that was good but not great. It can be difficult to extract value from the primary market when demand investor demand is voracious, as that type of environment can lead to less favorable pricing. Next week is expected to be on the lighter side with syndicate desks looking for $25bln in primary volume.

Flows

According to LSEG Lipper, for the week ended May 14, investment-grade bond funds reported an inflow of +$1.86bln. This broke a 7-week streak of trade-turmoil outflows. Total year-to-date flows into investment grade were +$6.649bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.