Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were -$0.2 billion and year to date flows stand at -$24.2 billion. New issuance for the week was $1.8 billion and year to date HY is at $60.0 billion, which is -28% over the same period last year.

(Bloomberg) High Yield Market Highlights

- Junk bond yields continued to head south as they dropped to a two-month low at close, with the biggest decline in more than seven weeks. Yields fell across ratings for three consecutive sessions.

- Spreads also tightened across ratings and saw the largest move in more than seven weeks as stocks continued to climb; the VIX dropped to a two-week low

- Strength and resilience of the market was also reflected in the pricing of two drive-by offerings amid 11 weeks of outflows from retail funds

- Two drive-by bond offerings were from the energy sector – Resolute Energy and Targa Resources; Targa Resources had orders of more than $3b and priced in the middle of talk

- Primary market priced four deals for $1.8b, which suggested junk bond investors were not heading to the exit

- While yields dropped and spreads tightened, junk investors have turned increasingly cautious and selective in credit-picking, a mood reflected in the pricing of American Greetings Corp yesterday

- AM was the second deal this week after McDermott International to price at a deep discount and offer double-digit yields

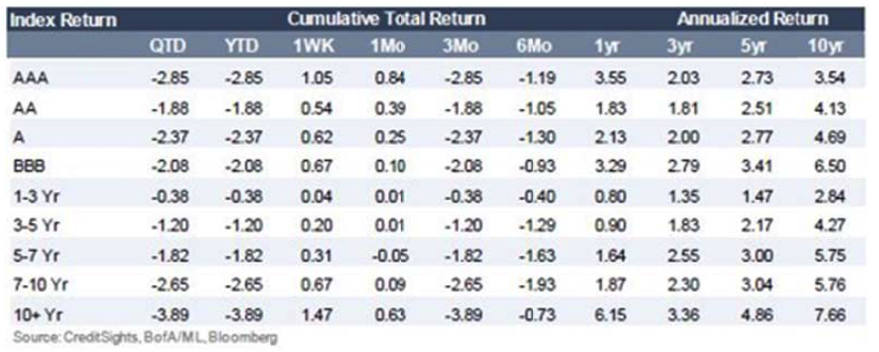

- CCCs continued to beat BBs and single-Bs with positive YTD returns of 0.55%

- CCCs still beat stocks and investment-grade bonds, with IG’s YTD returns negative 2.68%

- BBs were the worst with negative YTD returns of 1.41%, followed by single-Bs negative 0.24%

- The default rate should move lower in 2018 amid a growing economy and improving credit conditions in the commodity sector, Moody’s John Puchalla wrote in note

(Business Wire) Wireless Carrier Selects Zayo for Significant National Expansion

- A major wireless carrier has selected Zayo for fiber-to-the-tower (FTT) to new macro towers in 30 markets across 21 states. The deal is an expansion of an agreement announced in September 2016. Inclusive of both contracts, Zayo will connect thousands of macro towers for the customer. The contract is Zayo’s largest mobile infrastructure contract to date.

- The solution includes deployment of dark fiber infrastructure, in some cases replacing legacy Ethernet. The new infrastructure will support the carrier’s strategy of improving coverage and capacity across its network to accommodate increasing traffic and to prepare for 5G. The deployment will leverage Zayo’s existing fiber network and includes construction of hundreds of route miles of fiber.

- “This undertaking is the result of a trusted relationship with the customer,” said Dan Caruso, chairman and CEO of Zayo. “As they continue to densify to meet the growing demand for bandwidth, dark fiber provides the optimal long-term solution.”

- This agreement pertains to macro towers. Under other contracts, Zayo is deploying small cell infrastructure for this customer. In many cases, these are full turnkey implementations, including RF design, site acquisition, permitting and installation of equipment.

(Bloomberg) AMC Cinemas Tiptoes Into Saudi Arabia as Theater Ban Lifted

- AMC Entertainment, controlled by China’s Dalian Wanda, was granted the first cinema license in Saudi Arabia and plans to open 100 theaters with the country’s Public Investment Fund.

- AMC, the world’s largest exhibitor, and the Development & Investment Entertainment Co., a subsidiary of Saudi Arabia’s PIF, plan to open as many as 40 cinemas within five years and 60 more by 2030, according to a statement Wednesday from the Leawood, Kansas-based company.

- There are no commercial theaters in Saudi Arabia and plans to open them present challenges for the conservative kingdom, such as whether men and women can sit together and what types of movies will play. The partners are aiming for “50 percent market share of the Saudi Arabian movie theater industry,” the parties said. The first AMC in Saudi Arabia will open in the capital Riyadh on April 18.

- The announcement coincides with the U.S. visit by Crown Prince Mohammed bin Salman, who is looking to burnish his image as the leader of a more open Saudi economy.

(Modern Healthcare) Dialysis industry on alert as Calif. union pushes for reimbursement cap

- A California fight between dialysis clinics and a major hospital workers’ union has healthcare industry investors and stakeholders jittery as the union gets ready to push a ballot initiative to cap private insurance reimbursements for dialysis.

- The Service Employees International Union–United Healthcare Workers West, one of the country’s largest hospital workers’ unions, has gathered more than 600,000 voter signatures for a statewide ballot measure to cut off dialysis clinics’ commercial insurance reimbursement at 115% of care costs, which would slash their current rates.

- The union claims the proposal would pressure clinics to improve care for dialysis patients by reinvesting extra revenue into staffing and other efforts to raise standards in order to bump up the cost of care.

- But critics of the initiative say the measure could spur reverberating losses for corporate dialysis giants, hospitals and even state and federal coffers.

- Most of dialysis market in California belongs to Colorado-based DaVita Healthcare Partners and the German company Fresenius Medical Care, who have about 70% of the state market share. The 30% remaining market share belongs to independent or not-for-profit clinics. California has just under 600 dialysis clinics.

- California has an extra high rate of growth in dialysis patients — about 5% every year — and there are already more than 68,000 dialysis patients in the state.

- But SEIU members say dialysis clinic regulations are far too lax, and facilities have been plagued by issues like rat and cockroach infestations or staffing shortages that leave technicians with only minutes to clean up stations before another patient receives treatment.

- “With regards to staffing it’s a free-for-all,” said union member and longtime dialysis technician Emanuel Gonzales, who is helping to lead the union campaign and has worked in several dialysis centers across San Bernardino County and the Inland Empire in California. “They pretty much operate anyway they like. If something happens, they could blame workers.”

As we have stated in previous commentaries, we expect that, over the longer term, this trend will reverse, and those investors who have favored higher quality and avoided the temptation of “reaching for yield” will be rewarded with outperformance over a longer time horizon.

As we have stated in previous commentaries, we expect that, over the longer term, this trend will reverse, and those investors who have favored higher quality and avoided the temptation of “reaching for yield” will be rewarded with outperformance over a longer time horizon.

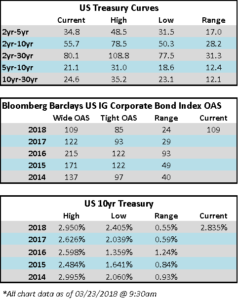

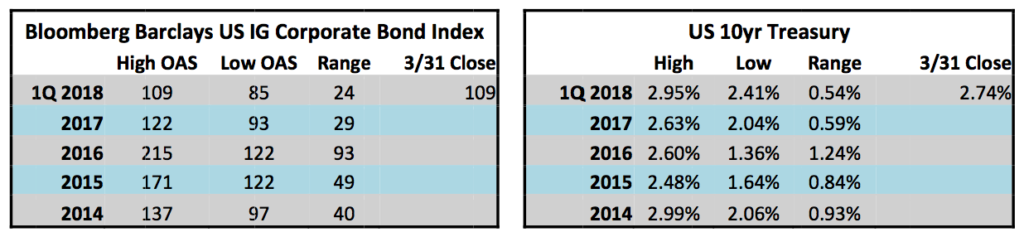

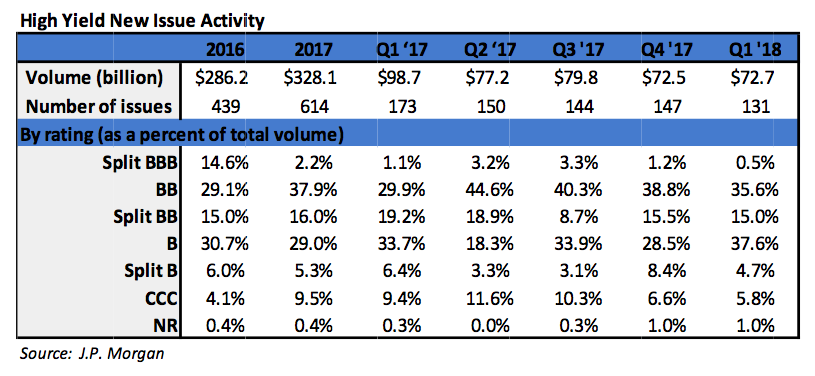

During the first quarter, the high yield primary market posted $72.7 billion in issuance. Importantly, almost three‐quarters of the issuance was used for refinancing activity. That was the highest level of refinancing since 2009. Issuance within Energy comprised just over a quarter of the total issuance. The 2018 first quarter level of issuance was relative to the $98.7 billion posted during the first quarter of 2017. The full year issuance for 2017 was $328.1 billion, making 2017 the strongest year of issuance since the $355.7 posted in 2014.

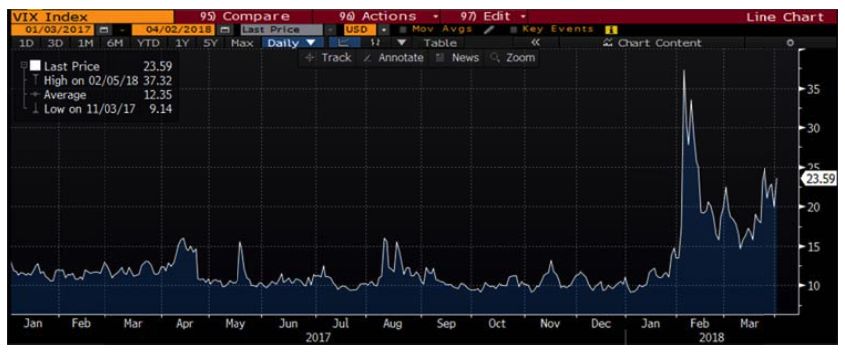

During the first quarter, the high yield primary market posted $72.7 billion in issuance. Importantly, almost three‐quarters of the issuance was used for refinancing activity. That was the highest level of refinancing since 2009. Issuance within Energy comprised just over a quarter of the total issuance. The 2018 first quarter level of issuance was relative to the $98.7 billion posted during the first quarter of 2017. The full year issuance for 2017 was $328.1 billion, making 2017 the strongest year of issuance since the $355.7 posted in 2014. The chart to the left is sourced from Bloomberg and is the Chicago Board Options Exchange Volatility Index (“VIX”). The VIX is a market estimate of future volatility in the S&P 500 equity index. It is quite clear that the market has entered a period of higher volatility. In fact, the equity market through the first quarter of 2018 is already much more volatile than all of 2017 as measured by the number of positive and negative 1% days.iv In addition to the volatility witnessed throughout the markets during the first quarter, there have been a few transitions in high profile government posts as well. Jerome Powell began a four‐year term as Chair of the Federal Reserve following the end of Janet Yellen’s single term in that role; economist Larry Kudlow succeeded to director of the National Economic Council after Gary Cohn’s resignation; and Mike Pompeo and John Bolten were nominated as Secretary of State and National Security Adviser, respectively, after Rex Tillerson and HR McMaster were dismissed from the roles.

The chart to the left is sourced from Bloomberg and is the Chicago Board Options Exchange Volatility Index (“VIX”). The VIX is a market estimate of future volatility in the S&P 500 equity index. It is quite clear that the market has entered a period of higher volatility. In fact, the equity market through the first quarter of 2018 is already much more volatile than all of 2017 as measured by the number of positive and negative 1% days.iv In addition to the volatility witnessed throughout the markets during the first quarter, there have been a few transitions in high profile government posts as well. Jerome Powell began a four‐year term as Chair of the Federal Reserve following the end of Janet Yellen’s single term in that role; economist Larry Kudlow succeeded to director of the National Economic Council after Gary Cohn’s resignation; and Mike Pompeo and John Bolten were nominated as Secretary of State and National Security Adviser, respectively, after Rex Tillerson and HR McMaster were dismissed from the roles. Being a more conservative asset manager, Cincinnati Asset Management remains significantly underweight CCC and lower rated securities. For the first quarter, that focus on higher quality credits was a detriment as our High Yield Composite gross total return underperformed the return of the Bloomberg Barclays US Corporate High Yield Index (‐1.83% versus ‐0.86%). The higher quality credits that were a focus tended to react more negatively to the interest rate increases. This was an additional consequence also contributing to the underperformance. Our credit selections in the food & beverage and home construction industries were an additional drag on our performance. However, our credit selections in the cable & satellite and leisure industries were a bright spot in the midst of the negative first quarter return.

Being a more conservative asset manager, Cincinnati Asset Management remains significantly underweight CCC and lower rated securities. For the first quarter, that focus on higher quality credits was a detriment as our High Yield Composite gross total return underperformed the return of the Bloomberg Barclays US Corporate High Yield Index (‐1.83% versus ‐0.86%). The higher quality credits that were a focus tended to react more negatively to the interest rate increases. This was an additional consequence also contributing to the underperformance. Our credit selections in the food & beverage and home construction industries were an additional drag on our performance. However, our credit selections in the cable & satellite and leisure industries were a bright spot in the midst of the negative first quarter return.