CAM High Yield Market Note

8/9/2019

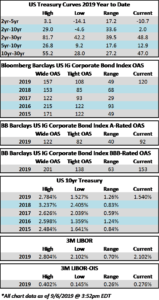

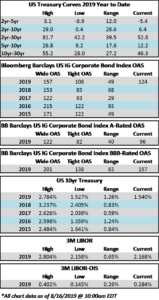

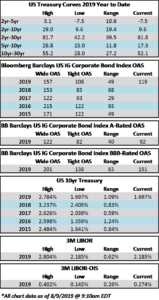

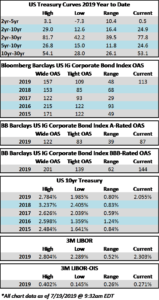

Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were -$3.6 billion and year to date flows stand at $11.9 billion. New issuance for the week was $4.4 billion and year to date HY is at $159.5 billion, which is +33% over the same period last year.

(Bloomberg) High Yield Market Highlights

- It’s a risk-off day for U.S. junk bonds as stock futures tumble on renewed trade worries. Recent market turmoil has rattled junk bond investors as they withdrew $3.6b from U.S. high yield funds, the biggest outflow since February of last year.

- Market volatility has started taking casualties as two issuers – – U.S. Farathane LLC and Sirius Minerals Plc — pulled high- yield offerings this week

- High-yield returns will come under pressure again today after rebounding Thursday on the heels of an equity rally to jump the most in seven weeks

- YTD returns stand at 9.865%, after a gain of 0.45% yesterday. This year’s peak was 10.6% in July

- BBs YTD returns stand at 11.01%

- Single-Bs YTD returns stand at 9.95%

- CCCs returns stand at 5.63%

- Yields dropped and spreads tightened across ratings

- Bloomberg Barclays index yield dropped 22bps to close at 6.05% and spreads narrowed 24bps to 416bps over U.S. Treasuries

- Yields on CCC rated debt, which has borne the brunt of the volatility, dropped 22bps to 10.62%. Spreads of 881bps over U.S. Treasuries are at their tightest in seven weeks

(Company Report) Arconic Reports Second Quarter 2019 Results

Highlights include:

- Revenue of $3.7 billion, up 3% year over year; organic revenue up 10% year over year

- Net loss of $121 million, or $0.27 per share, mainly driven by non-cash asset impairments of $357 million, versus net income of $120 million, or $0.24 per share, in the second quarter 2018

- Net income excluding special items of $269 million, or $0.58 per share, versus $185 million, or $0.37 per share, in the second quarter 2018

- Operating loss of $81 million, versus operating income of $324 million in the second quarter 2018

- Operating income excluding special items of $484 million, up 27% year over year

- Operating income margin excluding special items up 240 basis points year over year

- Cash balance of $1.4 billion, improved $38 million sequentiallyUpdated 2019 guidance:

- Revenue unchanged at $14.3-$14.6 billion

- Increased the midpoint of Earnings Per Share Excluding Special Items by 10%; increased the range from $1.75-$1.90 to $1.95-$2.05

- Increased Adjusted Free Cash Flow to $700-$800 million

- Added guidance for EBITDA Excluding Special Items at $2.25-$2.35 billion

Arconic Chairman and Chief Executive Officer John Plant said, “In the second quarter 2019, the Arconic team delivered improved quarterly revenue, adjusted operating income, adjusted operating income margin, and adjusted earnings per share on both a year-over-year and sequential basis. Based on our first half performance and our outlook for the remainder of 2019, we are increasing our full-year adjusted earnings per share and adjusted free cash flow guidance for the second time in 2019.”

(Company Report) TENNECO REPORTS SECOND QUARTER 2019 RESULTS

- Tenneco reported second quarter 2019 revenue of $4.5 billion, a 78% increase versus $2.5 billion a year ago, which includes $1.9 billion from acquisitions. On a constant currency pro forma basis, total revenue increased 1% versus last year, while light vehicle industry production declined 8% in the quarter. Value-add revenue for the second quarter was $3.7 billion.

- Second quarter 2019 adjusted net income was $97 million, or $1.20 per diluted share, compared with $96 million, or $1.84 per diluted share last year. Diluted shares outstanding in the second quarter increased 57% to 80.9 million shares, from 51.6 million shares in the second quarter 2018, primarily due to the acquisition of Federal-Mogul.

- Second quarter adjusted EBITDA was $414 million versus $233 million last year. Adjusted EBITDA as a percent of value-add revenue was 11.1%. Second quarter performance improved 240 basis points sequentially, compared to first quarter 2019, driven by the ramp up of synergy benefits and cost control initiatives. Cash generated from operations was $50 million.

- “Tenneco’s revenue growth outpaced industry production by nine percentage points, driven by higher light vehicle, commercial truck and off-highway revenues,” said Brian Kesseler, co-CEO, Tenneco. “We delivered sequential earnings improvement on flat revenue quarter to quarter, with disciplined cost management and effective synergy capture actions.”

- “In the third quarter, we expect our revenues to outgrow the markets we serve,” said Roger Wood, co-CEO Tenneco. “More importantly, we anticipate higher margins on a year-over-year basis in both divisions supported by operational performance improvements, synergy realization and our continued focus on eliminating waste and cost throughout the business.”

- The company confirmed its targeted timing for the separation of the business into two standalone companies, and expects the DRiV™ spinoff to occur mid-2020. Management remains focused and committed to the separation of the businesses.

(PR Newswire) TRANSDIGM GROUP REPORTS FISCAL 2019 THIRD QUARTER RESULTS

- Net sales of $1,658.3 million, up 69.1% from $980.7 million. Organic sales growth was 11.8%.

- Net income from continuing operations of $144.5 million, down 33.5% from $217.4 million

- Earnings per share from continuing operations of $2.57, down 34.3% from $3.91

- EBITDA As Defined of $691.0 million, up 41.8% from $487.1 million. EBITDA for the quarter was reduced by $16 million for the payment of a voluntary refund to several U.S. Department of Defense agencies.

- Adjusted earnings per share of $4.95, up 23.4% from $4.01

- Esterline net sales contribution of $545.3 million, EBITDA as Defined contribution of $134.4 million and implied EBITDA as Defined margin of 24.6%

- Upward revision to fiscal 2019 financial guidance. Increased EBITDA As Defined mid-point $90 million to $2,435 million. Increased adjusted earnings per share mid-point $1.28 per share to $18.09.

(Globe Newswire) CoreCivic Reports Second Quarter 2019 Financial Results

Highlights of Second Quarter 2019 vs. Second Quarter 2018:

- Total revenue of $490.3 million, an increase of 9%

- CoreCivic Safety revenue of $440.4 million, an increase of 7%

- CoreCivic Community revenue of $30.7 million, an increase of 24%

- CoreCivic Properties revenue of $19.1 million, an increase of 60%

- Normalized FFO per diluted share of $0.69, an increase of 21%

- Adjusted EBITDA of $115.3 million, an increase of 18%

- Damon T. Hininger, CoreCivic’s President and Chief Executive Officer, said, “During the second quarter we continued to see strong fundamental growth across each of our business segments, and we anticipate these growth trends will continue, as demonstrated by our updated financial guidance and further supported by our recently announced new contract awards.”

Based on current business conditions, the Company is providing the following financial guidance for the third quarter 2019 and the following updated guidance for the full year 2019:

- We have $325.0 million of senior unsecured notes maturing in April 2020. We currently have capacity under our revolving credit facility to repay these notes prior to their maturity, and expect to continue to have such capacity through maturity. We will also monitor the capital markets and may issue debt securities or obtain other forms of capital if, and when we determine that market conditions are favorable, utilizing the net proceeds to refinance such notes.