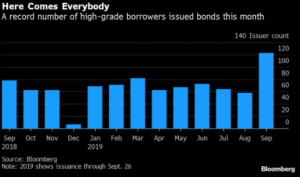

Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were -$0.1 billion and year to date flows stand at $17.0 billion. New issuance for the week was $1.1 billion and year to date HY is at $199.5 billion, which is +30% over the same period last year.

(Bloomberg) High Yield Market Highlights

- The U.S. high-yield bond market is set to extend its first weekly gain in three weeks as trade-talk optimism boosts stock futures and after reports of a missile attack on an Iranian tanker pushed the price of Brent crude to $60 per barrel.

- Junk bonds posted gains for the second straight session on Thursday, with the Bloomberg Barclays U.S. high-yield index up 0.08% this week and 10.97% YTD; yields have dropped one basis point this week to 5.89%

- BBs gained 0.03% to take YTD returns to 12.615% and yields dropped to close at 4.20%

- Single-B yields saw the biggest drop in more than three weeks on Thursday to close at 5.98%, with YTD climbing to 11.294%

- CCC yields jumped to a more than eight-month high of 11.17% while returns rose by 0.05% to take the YTD to 4.51%

- Sentiment remains cautious as investors pulled cash from U.S. high-yield funds

- The primary market activity gained pace yesterday after a sluggish start to the week, pricing three deals

(The Philadelphia Inquirer) Aramark has a new CEO, activist investor becomes vice chair of the board

- Aramark Corp. on Monday named John J. Zillmer, an executive associated with an activist investor who controls 20% of the Philadelphia company, chief executive, replacing Eric Foss.

- The food- and uniform-services giant also announced a revamped board of directors, with the appointment of five new independent directors, all with consumer goods and food industry experience.

- Zillmer had previously spent 18 years at Aramark, rising to be president of global food & support services before departing in 2004. After leaving Aramark, Zillmer, 64, served as CEO of Allied Waste Industries and Univar Solutions, a global chemical and ingredients distributor.

- “I am extremely excited about the opportunity to rejoin Aramark at such a dynamic time in the company’s history,” Zillmer said in a news release. “I look forward to working closely with the board and the Aramark team to drive growth and value for our employees, customers, partners, and shareholders.”

- Even though Zillmer left Aramark in 2004, he has maintained his residency in Philadelphia. Current and former Aramark employees who know Zillmer from his previous time at the company said they were pleased to have him back and confident that he would take the company in the right direction.

- Paul C. Hilal, whose Mantle Ridge L.P. is Aramark’s largest shareholder, will be vice chairman. Hilal and Zillmer both serve on the board of CSX Corp., another of Hilal’s targets. Zillmer is non-executive chairman of CSX’s board. Zillmer also joined Aramark’s board, where Steve Sadove remains chairman.

- The moves come six weeks after Foss abruptly retired from the Philadelphia company, shortly after activist investor Hilal disclosed that Mantle Ridge had acquired 9.8% of Aramark’s shares and additional interest that gives Mantle Ridge 20% of the company.

(Reuters) Trump says U.S., China have reached substantial phase-1 trade deal

- S. President Donald Trump on Friday outlined the first phase of a deal to end a trade war with China and suspended a threatened tariff hike, but officials on both sides said much more work needed to be done before an accord could be agreed.

- The emerging deal, covering agriculture, currency and some aspects of intellectual property protections, would represent the biggest step by the two countries in 15 months to end a tariff tit-for-tat that has whipsawed financial markets and slowed global growth.

- But Friday’s announcement did not include many details and Trump said it could take up to five weeks to get a pact written.

- He acknowledged the agreement could fall apart during that period, though he expressed confidence that it would not.

- “I think we have a fundamental understanding on the key issues. We’ve gone through a significant amount of paper, but there is more work to do,” U.S. Treasury Secretary Steven Mnuchin said as the two sides gathered with Trump at the White House. “We will not sign an agreement unless we get and can tell the president that this is on paper.”

- With Chinese Vice Premier Liu He sitting across a desk from him in the Oval Office after two days of talks between negotiators, the president told reporters that the two sides were very close to ending their trade dispute.

- China’s official state-owned news organization Xinhua said that both sides “agreed to make the efforts towards a final agreement.”

- Trump, who is eager to show farmers in political swing states that he has their backs, lauded China for agreeing to buy as much as $50 billion in agricultural products. But he left tariffs on hundreds of billions of dollars of Chinese products in place.

(Bloomberg) The Repo Market’s a Mess. (What’s the Repo Market?): QuickTake

(Bloomberg) The Repo Market’s a Mess. (What’s the Repo Market?): QuickTake