In the fourth quarter of 2021, the Bloomberg Barclays US Corporate High Yield Index (“Index”) return was 0.71% bringing the year to date (“YTD”) return to 5.28%. The CAM High Yield Composite net of fees total return was 0.45% bringing the YTD net of fees return to 4.03%. The S&P 500 stock index return was 11.02% (including dividends reinvested) for Q4, and the YTD return stands at 28.68%.

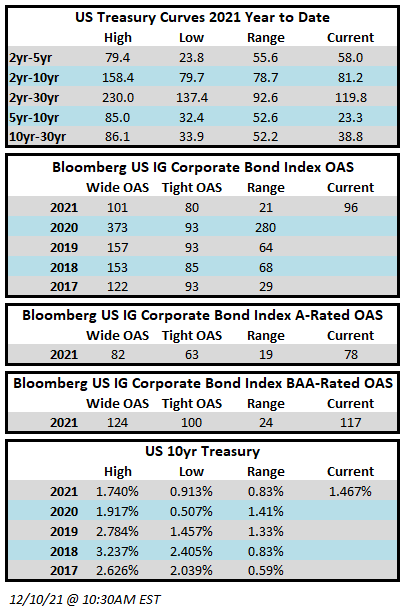

The 10 year US Treasury rate (“10 year”) was mostly range bound finishing at 1.51%, up 0.02% from the beginning of the quarter. Over the period, the Index option adjusted spread (“OAS”) tightened 6 basis points moving from 289 basis points to 283 basis points. The top two quality segments of the High Yield Market participated in the spread tightening as BB rated securities tightened 9 basis points and B rated securities tightened 14 basis points, while the CCC rated securities widened 25 basis points. Take a look at the chart below from Bloomberg to see a visual of the spread moves in the Index over the past five years. The graph illustrates the speed of the spread move in both directions during 2020 and the continuation of lower spreads in the first half of 2021. The OAS record low (not shown) is 233 basis points set back in 2007.

The Energy, Other Industrial, and Finance Companies sectors were the best performers during the quarter, posting returns of 1.56%, 1.38%, and 1.23%, respectively. On the other hand, Communications, Banking, and REITs were the worst performing sectors, posting returns of -0.24%, 0.05%, and 0.27%, respectively. Clearly the market was strong as only one sector posted a negative return in the period. At the industry level, auto, midstream, life insurance, and independent energy all posted the best returns. The auto industry posted the highest return 2.17%. The lowest performing industries during the quarter were cable, media, wirelines, and retailers. The cable industry posted the lowest return -0.66%.

The energy sector performance has continued to remain strong. Crude oil had a $20 per barrel range in Q4 and averaged $77 per barrel. Meanwhile, the natural gas market moved lower throughout the quarter coming down off highs not seen in three years. OPEC+ recently had a meeting and decided to further raise production levels.i The group has “restarted about two-thirds of the production they halted in 2020, and are seeking to drip-feed the remainder at a pace that will satisfy the recovery in fuel consumption — and stave off any inflationary price spike — without sending the market into a new slump. So far they’ve succeeded, with international crude prices trading near $78 a barrel.” OPEC has also chosen a new Secretary General that will take over in August as the group’s public face. The outgoing Secretary General will step down after completing a full term as permitted by governing rules.

During the fourth quarter, the high yield primary market continued at a strong pace posting $84.3 billion in issuance and making 2021 a record year. After two very active years for issuance, 2022 is likely to take a breather but the expectation is still in the ballpark of $400 billion. The issuance in Consumer Discretionary continued to be very strong with approximately 19% of the total during the quarter. Second place was broad based as Communications, Energy, and Financials each made up 14% of the total new paper placed in the market.

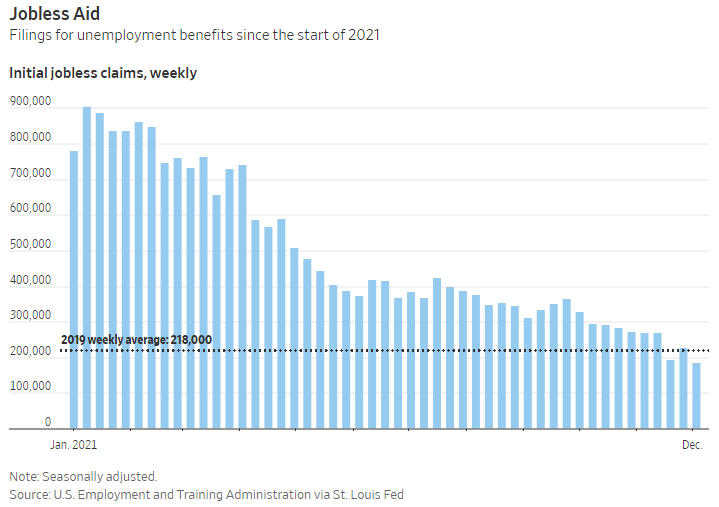

The Federal Reserve maintained the Target Rate to an upper bound of 0.25% at both the meetings in November and December. The chart to the left shows the updated Fed dot plot post the December meeting. Of note, the Fed median Target Rate for 2022 increased from 0.25 to 0.875, and the median increased for 2023 from 1.00 to 1.625. Additionally, at the December meeting the Fed agreed to accelerate the taper pace of their asset purchases. The change in the taper pace sets in place a plan for the program to end in March of 2022. The Fed has previously spoken of the desire to end the taper before starting Target Rate hikes. These moves are being driven by a tight employment market and inflation that is running higher than any point in the last 30 years. “There’s a real risk now, I believe, that inflation may be more persistent and…the risk of higher inflation becoming entrenched has increased,” said Mr. Powell at a news conference after the December meeting.

“That’s part of the reason behind our move today, is to put ourselves in a position to be able to deal with that risk.”ii

Intermediate Treasuries increased 2 basis points over the quarter, as the 10-year Treasury yield was at 1.49% on September 30th, and 1.51% at the end of the fourth quarter. The 5-year Treasury increased 29 basis points over the quarter, moving from 0.97% on September 30th, to 1.26% at the end of the fourth quarter. Intermediate term yields more often reflect GDP and expectations for future economic growth and inflation rather than actions taken by the FOMC to adjust the Target Rate. The revised third quarter GDP print was 2.3% (quarter over quarter annualized rate). Looking forward, the current consensus view of economists suggests a GDP for 2022 around 3.9% with inflation expectations around 3.5%.iii

Being a more conservative asset manager, Cincinnati Asset Management Inc. does not buy CCC and lower rated securities. This policy generally served our clients well in 2020. However, the lowest rated segment of the market outperformed during 2021. Thus, our higher quality orientation was not optimal for the year. As a result and noted above, our High Yield Composite net of fees total return did underperform the Index YTD. Our Composite also underperformed over the fourth quarter measurement period. A sizeable contributor was the Index strong performance in the under one year and over ten year duration buckets. These are both areas that our strategy tends not to participate in any meaningful way. Further, with the market staying strong during the fourth quarter, our cash position remained a drag on overall performance. Outside of that, credit selection drove much of the story in Q4. The downside was driven by selections in the energy sector and retailer industry, while the top positive offsets were found within the homebuilders and wireline industries.

The Bloomberg Barclays US Corporate High Yield Index ended the fourth quarter with a yield of 4.21%. The market yield is an average that is barbelled by the CCC rated cohort yielding 6.82% and a BB rated slice yielding 3.30%. Equity volatility, as measured by the Chicago Board Options Exchange Volatility Index (“VIX”), had an average of 19 over the quarter with a spike to a high of 35 as the market was coming to grips with the omicron variant. For context, the average was 15 over the course of 2019 and 29 for 2020. The fourth quarter had one bond issuer default on their debt. The trailing twelve month default rate fell to 0.27%.iv The current default rate is relative to the 6.17%, 4.80%, 1.63%, 0.92% default rates from the previous four quarter end data points listed oldest to most recent. Pre-Covid, fundamentals of high yield companies had been mostly good and in the aggregate fundamentals are back to those pre-covid levels. From a technical view, fund flows were roughly flat in October, negative in November, and positive in December. The 2021 year-end outflow stands at $4.8 billion.v In spite of this outflow, a strong bid remains in the market for high yield paper, and the declining default rate is keeping a risk on attitude in place for market participants. We are of the belief that for clients that have an investment horizon over a complete market cycle, high yield deserves to be considered as part of the portfolio allocation.

Covid, then delta, now omicron….the hits just keep on coming. All things considered, the market did very well this year. This is no doubt in part due to Congress and the Fed supplying trillions of dollars of support in response to the pandemic. November was indeed a tough month as market participants dealt with news of an emerging new variant. Many naturally sensed a buying opportunity as December was quite strong posting the best monthly return for the year. Participants surely understood that we are no longer in March 2020 operating largely in the dark and full of uncertainty. Uncertainty will always be a factor in the equation, but today we are much better prepared to deal with the ongoing pandemic. The vaccine has been rolled out and according to the CDC, 86% of the US population ages 18+ has received at least one shot. We now have boosters and emergency use pills approved. As cases continue to climb, signs point to much less severe outcomes.vi Additionally, companies are generally in good financial shape. As a country, we are currently in a place where the economy is booming and inflation is escalated. That is the backdrop as we move into 2022. Clearly, it is important that we exercise discipline and selectivity in our credit choices moving forward. We are very much on the lookout for any pitfalls as well as opportunities for our clients. We will continue to carefully monitor the market to evaluate that the given compensation for the perceived level of risk remains appropriate on a security by security basis. As always, we will continue our search for value and adjust positions as we uncover compelling situations. Finally, we are very grateful for the trust placed in our team to manage your capital.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results. Gross of advisory fee performance does not reflect the deduction of investment advisory fees. Our advisory fees are disclosed in Form ADV Part 2A. Accounts managed through brokerage firm programs usually will include additional fees. Returns are calculated monthly in U.S. dollars and include reinvestment of dividends and interest. The index is unmanaged and does not take into account fees, expenses, and transaction costs. It is shown for comparative purposes and is based on information generally available to the public from sources believed to be reliable. No representation is made to its accuracy or completeness.

i Bloomberg January 4, 2022: OPEC+ Agrees to Revive More Output

ii The Wall Street Journal December 15, 2021: Fed Officials Project Three Interest Rate Rises in 2022

iii Bloomberg January 4, 2022: Economic Forecasts (ECFC)

iv JP Morgan January 3,, 2022: “Default Monitor”

v Wells Fargo January 3, 2022: “Credit Flows”

vi Bloomberg January 4, 2022: Omicron Spares US ICUs So Far, Mirroring S. Africa Trajectory