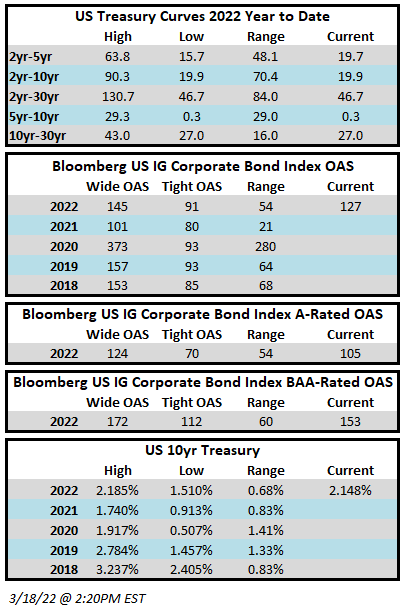

Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were -$2.4 billion and year to date flows stand at -$27.1 billion. New issuance for the week was $1.0 billion and year to date issuance is at $36.4 billion.

(Bloomberg) High Yield Market Highlights

- U.S. junk bonds are poised to post the biggest weekly gains in almost three months after Fed Chair Jerome Powell highlighted the strength of the economy, fueling the largest three-day rally in equities since November 2020.

- As the Federal Reserve began what is likely to be its most aggressive rate-hike campaign in two decades, Powell said the economy was strong and well-positioned to withstand tighter monetary policy.

- Still, “a sustained rally will require more clarification about peak inflation and the economic ramifications of the ongoing Russia-Ukraine war,” Barclays’ strategists Brad Rogoff and Dominique Toublan wrote on Friday.

- The rates curve indicates that persistently higher inflation will lead to higher short-term rates and could weigh on longer-term growth prospects, Barclays wrote.

- The gains in high-yield debt were across the board, with CCCs, the riskiest part of the market, on track to close the week with the biggest advance in three months after rallying for two straight sessions.

- Junk bond yields dropped 17bps to 6.12% on Thursday and spreads tightened 17bps to +369.

- BB yields dropped 16bps to close at 5.01%, the biggest one-day fall in more than three months.

- The Ba index posted gains of 0.69% on Thursday, and is likely to see the biggest weekly returns in three months, with gains of 0.4% so far.

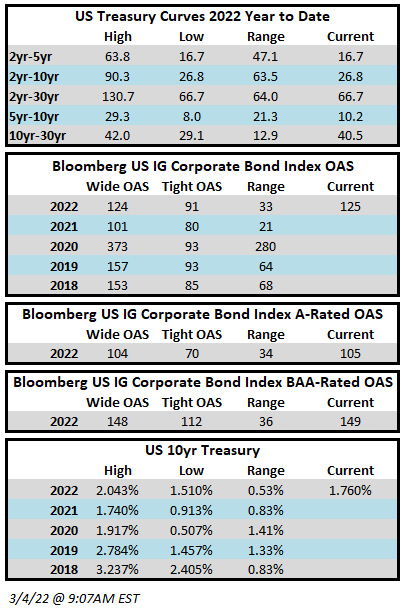

- The primary market was still quiet as borrowers wait for the markets to settle down after the FOMC decision to raise rates by 25bps, while indicating further 25bps hikes at each of the next six meetings.

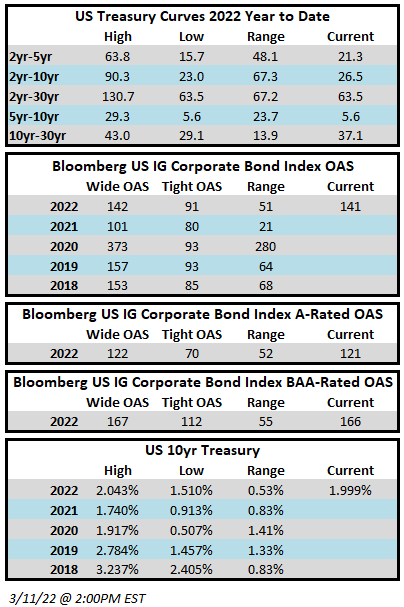

- The issuance volume stands at $36b year-to-date, the slowest first quarter since 2016, according to data compiled by Bloomberg.

(Bloomberg) Fed Lifts Rates a Quarter Point and Signals More Hikes to Come

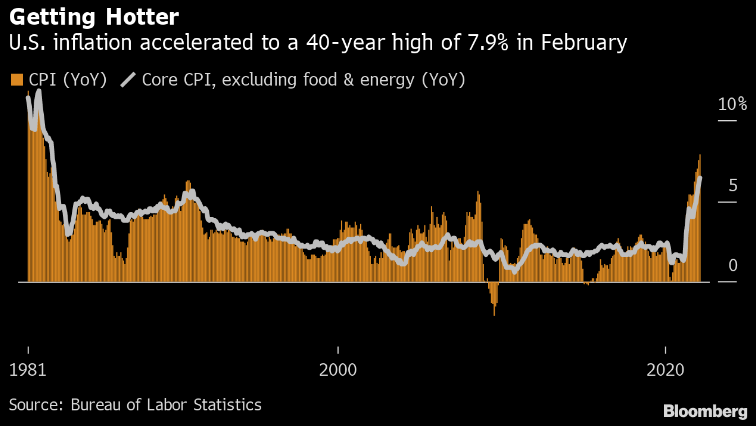

- The Federal Reserve raised interest rates by a quarter percentage point and signaled hikes at all six remaining meetings this year, launching a campaign to tackle the fastest inflation in four decades even as risks to economic growth mount.

- Policy makers led by Chair Jerome Powell voted 8-1 to lift their key rate to a target range of 0.25% to 0.5%, the first increase since 2018, after two years of holding borrowing costs near zero to insulate the economy from the pandemic. St. Louis Fed President James Bullard dissented in favor of a half-point hike, the first vote against a decision since September 2020.

- “The American economy is very strong and well positioned to handle tighter monetary policy,” Powell told a press conference Wednesday following a meeting of the Federal Open Market Committee. “I saw a committee that is acutely aware of the need to return the economy to price stability.”

- The hike is likely the first of several to come this year, as the Fed said it “anticipates that ongoing increases in the target range will be appropriate,” and Powell repeated his pledge to be “nimble.”

- In the Fed’s so-called dot plot, officials’ median projection was for the benchmark rate to end 2022 at about 1.9% — in line with traders’ bets but higher than previously anticipated — and then rise to about 2.8% in 2023.

- “The invasion of Ukraine by Russia is causing tremendous human and economic hardship,” the FOMC said in its policy statement following the two-day meeting in Washington, the first held in person — rather than via videoconference — since the pandemic began. “The implications for the U.S. economy are highly uncertain, but in the near term the invasion and related events are likely to create additional upward pressure on inflation and weigh on economic activity.”

- The Fed said it would begin allowing its $8.9 trillion balance sheet to shrink at a “coming meeting” without elaborating. Powell said officials had made good progress this week in nailing down their plans and could be in a position to begin the process at their May meeting, though the FOMC had not taken a decision to do so. The purchases of Treasuries and mortgage-backed securities, which concluded this month, were intended to provide support to the economy during the Covid-19 crisis and shrinking the balance sheet accelerates the removal of that aid.

- In new economic projections, Fed officials said they see inflation significantly higher than previously anticipated, at 4.3% this year, but still coming down to 2.3% in 2024. The forecast for economic growth in 2022 was lowered to 2.8% from 4%, while unemployment projections were little changed.

- The pivot to tighter monetary policy is sharper than policy makers expected just three months ago, when their median projection was for just three quarter-point rate increases this year.

- The Fed previously held off from raising rates as officials bet the inflation shock would fade once the economy returned to normal following the pandemic recession and lockdowns, though they were also cautious amid new Covid-19 variants and data showing a choppy jobs recovery.

- Instead, price gains accelerated amid a mixture of massive government stimulus, tightening labor markets, surging commodity costs and frayed supply chains. Powell has also been operating under a Fed policy framework, adopted in mid-2020, to allow some above-target inflation in the hope of broadening employment.

- President Joe Biden has called taming inflation his top economic priority, while fellow Democrats worry failure to restrain prices could cost them their thin congressional majorities in November’s midterm elections.