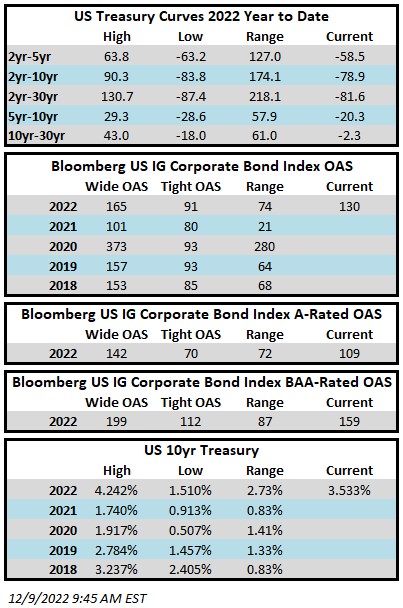

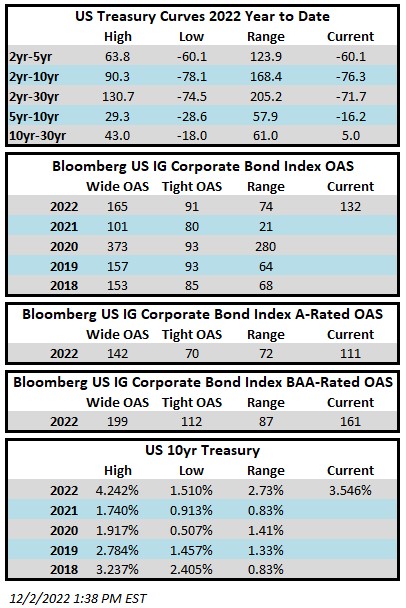

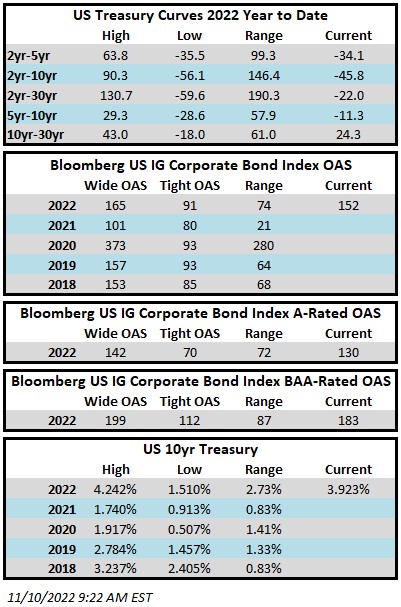

Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were -$0.6 billion and year to date flows stand at -$48.5 billion. New issuance for the week was $2.2 billion and year to date issuance is at $104.9 billion.

(Bloomberg) High Yield Market Highlights

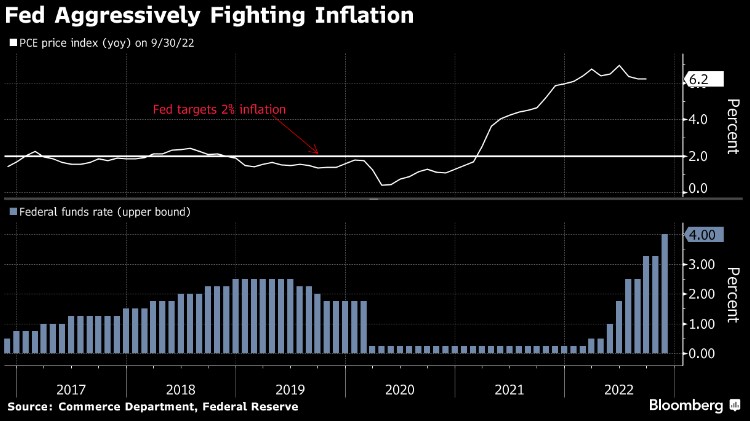

- U.S. junk bonds snapped a six-day rally as yields surged 13bps to 8.45%, marking the biggest one-day loss in more than five weeks, after central banks signaled more rate hikes are needed to cool the rate of inflation. Fed Chair Jerome Powell reiterated the central bank’s hawkish stance and said the bank is not close to ending its rate-hike campaign to tame inflation, a sentiment echoed by European Central Bank President Christine Lagarde.

- The hawkish tilts from the FOMC and ECB reversed the more positive sentiment earlier in the week spurred by a slowdown in the consumer-price index, Barclays’s Bradley Rogoff wrote on Friday.

- Bloomberg economists Anna Wong, David Wilcox and Eliza Winger wrote that the most striking part of the updated economic projections by the Federal Reserve “is how unified the committee is on the need to raise rates more aggressively – significantly higher than the 4.8% terminal rate markets had priced in ahead of the meeting.”

- The losses spanned across all high yield ratings. BB yields rose 11bps to 6.77%, the biggest one- day jump in four weeks. The BB index posted the biggest one-day loss in more than five weeks and ended a six-day gaining streak.

- CCC yields rose 13bps to 13.79%. The index posted a loss of 0.37% on Thursday, the most in more than two weeks, after gaining for five straight sessions.

- The junk bond primary market has ground to a halt, with just a little over $2b in new bond sales month-to-date, the slowest since December 2018. The rest of the year is expected to be quiet on the new issue front as investors work on the year- end closings.

(Bloomberg) Powell Says Fed Still Has a ‘Ways to Go’ After Half-Point Hike

- Chair Jerome Powell said the Federal Reserve is not close to ending its anti-inflation campaign of interest-rate increases as officials signaled borrowing costs will head higher than investors expect next year.

- “We still have some ways to go,” he told a press conference on Wednesday in Washington after the Federal Open Market Committee raised its benchmark rate by 50 basis points to a 4.25% to 4.5% target range.

- Powell said that the size of the rate increase delivered on Feb. 1 at the Fed’s next meeting would depend on incoming data — leaving the door open to another half-percentage point move or a step down to a quarter point — and he pushed back against bets that the Fed would reverse course next year.

- “I wouldn’t see us considering rate cuts until the committee is confident that inflation is moving down to 2% in a sustained way,” he said. “Restoring price stability will likely require maintaining a restrictive policy stance for some time,” he said.

- “The committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2% over time,” the FOMC said in its statement, repeating language it has used in previous communications.

- “It is our judgment today that we are not at a sufficiently restrictive policy stance yet,” the Fed chief said. “We will stay the course until the job is done.”

- Powell had previously signaled plans to moderate hikes, while emphasizing that the pace of tightening is less significant than the peak and the duration of rates at a high level.

- The decision follows four consecutive 75 basis-point hikes that have boosted rates at the fastest pace since Paul Volcker led the central bank in the 1980s.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.