It was a difficult week for the Corporate Bond market as fear and uncertainty related to COVID-19, a precipitous drop in oil, and an inter-meeting rate cut by the U.S. Federal Reserve drove Treasuries lower and spreads wider.

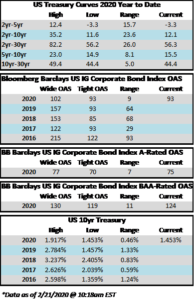

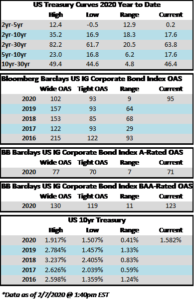

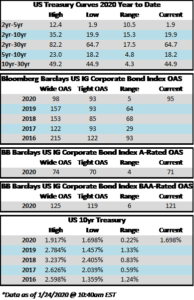

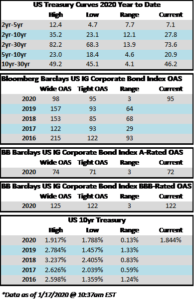

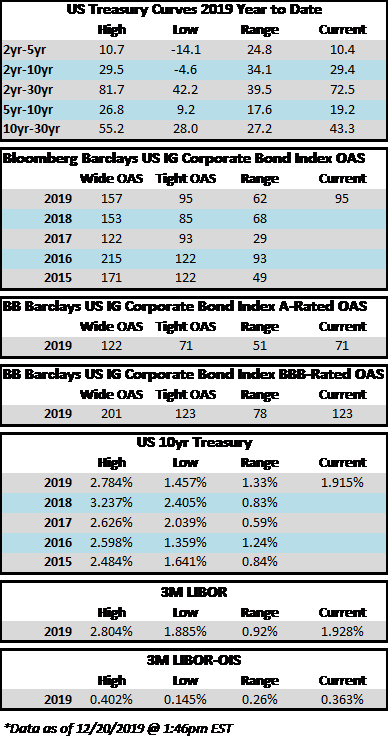

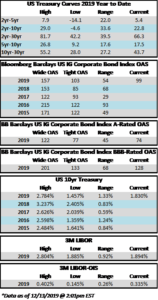

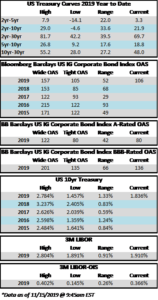

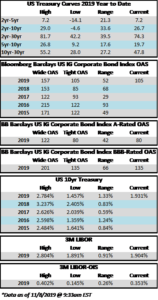

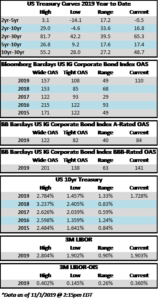

When we look at the Investment Grade market the option adjusted spread on the Bloomberg Barclays US Corporate Index was 122 at month-end February 2020, while on Friday, March 13, 2020 it closed at 216. This was one of the quickest and most volatile spread moves in the history of the investment grade credit market.

There was a corresponding move lower in Treasuries across the board – this helped to mitigate some, but not all, of the impact of widening spreads.

To provide some context on the performance of the investment grade credit market, through the end of the day on Friday March 13, the Bloomberg Barclays US Corporate Index posted a YTD gross total return of -1.88%. Comparatively, the S&P 500 YTD gross total return was -15.73% (Source: Bloomberg). While we are not happy to see negative returns in the corporate bond market, the asset class has performed as expected during a period of extreme volatility, and it has held up materially better than equities and other risk assets.

CAM does not provide intra-monthly performance figures, however as of March 13, 2020 we note that CAM’s portfolio has the following defensive characteristics relative to the Index. CAM is significantly underweight in BBB rated corporate credit relative to the Index. CAM caps its exposure to BBB-rated credit at 30% while the Corporate Index’s exposure was 49.14% as of March 13. Interestingly, the BBB concentration of the Index is down slightly YTD but that is merely because some large issuers, like Kraft-Heinz, were downgraded from BBB to junk status – an example of the type of investment CAM seeks to avoid through its bottom up research process. The second and third major factors that will impact CAM’s performance relative to the Index relate to individual credit selection and avoidance of certain industries which have been particularly hard hit by COVID-19, such as Leisure. To be sure, we have individual credits within our portfolio that have been affected by both COVID-19 and the decline in the oil market and we are constantly monitoring and evaluating those situations through active management of the portfolio.

It was also an exceptionally difficult week for the High Yield market with a one-two punch of fear and uncertainty related to COVID-19 as well as a complete flush of the oil market due to the lack of an OPEC agreement. The option adjusted spread on the Bloomberg Barclays US Corporate High Yield Index spiked above 700 for the first time since the commodity fueled rout of 2016. The Index YTD gross total return was -8.84% through the end of Friday March 13 (Source: Bloomberg).

Again, CAM does not provide intra-monthly performance figures, but our High Yield portfolio has the following defensive characteristics relative to the Index. CAM had over 10% of its portfolio in cash at the start of the current sell-off in February and CAM is underweight, or zero weight, some sectors of the market that were particularly hard hit by this sell off, such as Oil Field services. To be sure, our portfolio’s gross total return was negative as of February 29, 2020, and subsequent drawdown has been widespread. We have a number of credits that have experienced increased volatility and as always we are closely monitoring those situations as well as all the credits in our portfolio. Currently, we are comfortable with the individual credit metrics of our holdings and we believe the overall portfolio is well positioned should the economy enter a recessionary environment. Our cash balance also affords us the ability to be opportunistic on behalf of our clients as those situations arise.

The High Yield market can be extremely volatile in times of stress. It is not as deep or as liquid as the Investment Grade credit market and that is one of the reasons that spreads can gap wider so quickly. The growth of ETFs has exacerbated this problem as they are often forced to sell in the face of investor liquidations. We would caution that during times like these it can be difficult to achieve favorable pricing when looking to sell a high yield security; and depending on your risk tolerance it can often be a good opportunity to buy. We ask that our investors continue to trust that we will professionally manage your portfolios with a long-term objective and through the extent of the current downturn to the best of our ability.

We believe it is important in times like these to remind our investors of our investment philosophy and process at CAM. While volatile markets present challenges as well as opportunities, the way we manage money remains very consistent. We are conservative investors of domestic corporate bonds with a “bottom-up value” investment discipline, stressing first and foremost the preservation of capital, with an important secondary focus on total return. We seek to deliver these results by identifying quality businesses that we are comfortable owning in all markets.

We take the responsibility of managing your money very seriously and we will always do our best to perform that task to the highest standard of care. We sympathize with our clients in uncertain times such as these and we hope that you and your families stay safe and healthy.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. High Yield bonds present risks specific to below investment grade fixed income securities. Valuation may result in uncertainties and greater volatility, less liquidity, widening credit spreads, and a lack of price transparency. Investments in fixed income securities may be affected by changes in the creditworthiness of the issuer and are subject to nonpayment of principal and interest. The value of fixed income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. Past performance is not a guarantee of future results. Gross of advisory fee performance does not reflect the deduction of investment advisory fees. Our advisory fees are disclosed in Form ADV Part 2A. Accounts managed through brokerage firm programs usually will include additional fees. Returns are calculated monthly in U.S. dollars and include reinvestment of dividends and interest. The Index is unmanaged and does not take into account fees, expenses, and transaction costs. It is shown for comparative purposes and is based on information generally available to the public from sources believed to be reliable. No representation is made to its accuracy or completeness.

The information provided in this report should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed do not represent an account’s entire portfolio and in the aggregate may represent only a small percentage of an account’s portfolio holdings. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable, or that the investment decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.