Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were -$6.4 billion and year to date flows stand at -$40.6 billion. New issuance for the week was $2.7 billion and year to date issuance is at $68.0 billion.

(Bloomberg) High Yield Market Highlights

- U.S. junk bonds are headed toward the biggest weekly loss in more than two years as yields jump to a 26-month high of 8.56% amid fears that the 75 basis points hike in interest rates by the Federal Reserve, the biggest since 1994, could trigger a recession.

- High-frequency credit card data shows that consumer spending growth has started to fade, suggesting more weakness in risk assets, Brad Rogoff of Barclays wrote on Friday.

- With the Federal Reserve focused on inflation and willing to take collateral risk, downside risk worsens, Barclays wrote.

- However, high yield will trade in the +450 to +475bps range, despite periods of overshooting, Barclays’ analysts wrote.

- The spreads breached the +500 mark to close at +508bps, the widest since November 2020 amid a broader risk-off move.

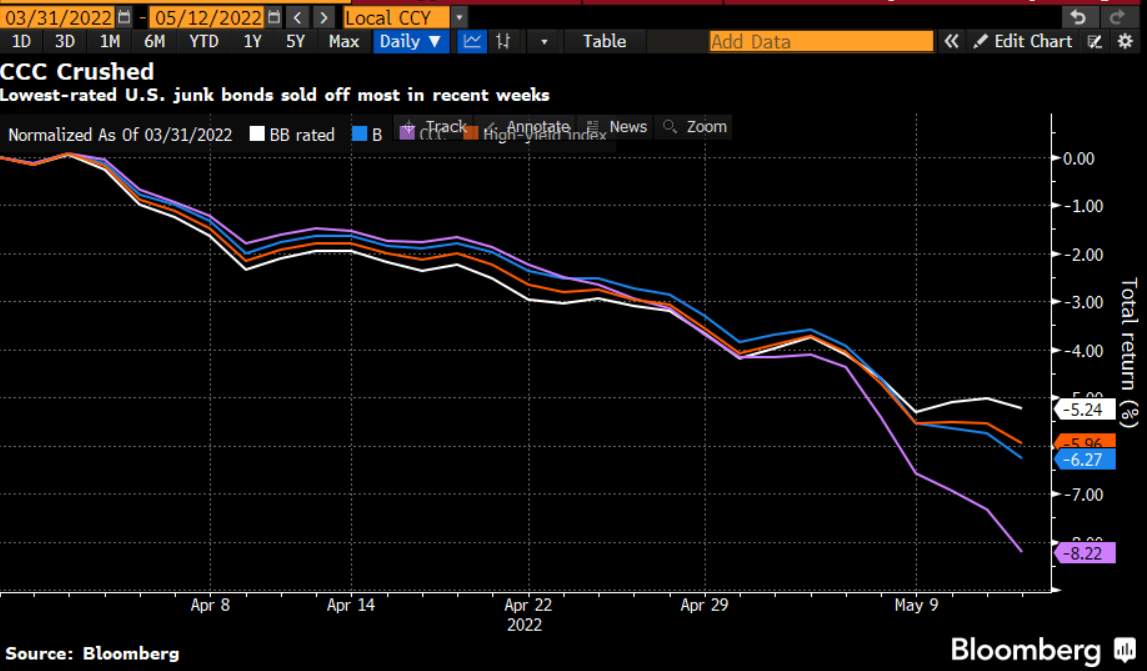

- The losses spanned across high-yield ratings amid growing concern that a recession could fuel a rapid increase in credit risk.

- CCCs, the riskiest of junk bonds, are also expected to see the most weekly loss since April 2020, with week-to-date losses at 3.01%.

- CCC yields rose to 12.88%, the highest since May 2020.

- The broader junk bond index is on track to post losses for the third straight week, with week-to-date losses at 3.09%, the most in a week since March 2020.

- The steady risk aversion was becoming evident in the primary market with several new issues pricing at a steep discount.

- The primary market was fairly quiet this week. The month-to-date tally stood at $9.3b, down 63% from comparable period last year.

- Junk bonds will wait and watch as US equity futures rebound cautiously along with stocks in Europe after a rout triggered by fears of an economic downturn as major central banks close the liquidity taps.

(Bloomberg) Powell Sets Path to Restrain Economy and Stop Runaway Inflation

- Federal Reserve Chair Jerome Powell took a step toward assuming the mantle of inflation slayer Paul Volcker, all but acknowledging that reining in run-away price pressures may result in a recession.

- Declaring that it’s essential to bring inflation down, Powell engineered the central bank’s biggest interest-rate increase since 1994 on Wednesday and held out the distinct possibility of another jumbo three-quarter percentage point increase in July.

- He openly endorsed for the first time raising rates well into restrictive territory with the aim of cooling off the labor market and pushing joblessness up — a strategy that in the past has often resulted in an economic downturn.

- “This is a Volcker-esque Fed,” said Diane Swonk, chief economist at Grant Thornton LLP. “That means the Fed is willing to take a rise in unemployment and a recession to avert a repeat of mistakes of the 1970s. Supply shocks won’t correct themselves, so the Fed must reduce demand to meet a supply constrained world.”

- The shift in stance carries perils not only for the economy, but for financial markets and President Joe Biden. Stocks have tumbled in recent months as the Fed has tightened credit to get on top of inflationary pressures that have proved more persistent and widespread than it expected.

- Biden has seen his popularity plunge as inflation has soared. A recession — and the higher unemployment that would bring — would rob the president of one of his few talking points in touting the benefits of his policies for the economy.

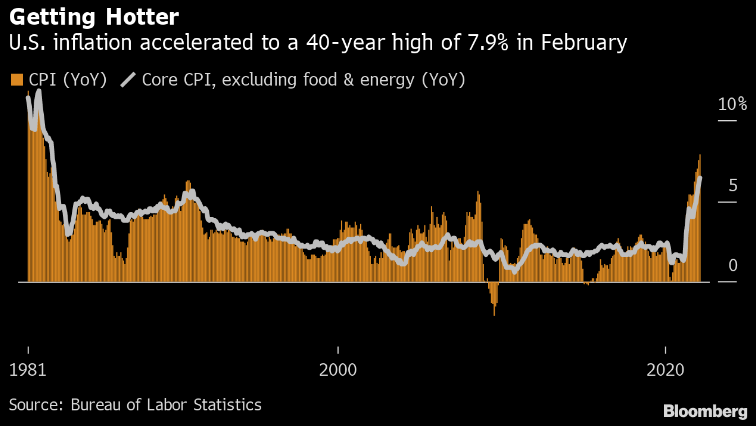

- An increasing number of economists are projecting a downturn next year as the Fed struggles to get on top of inflation that’s running at its highest level in four decades. Nearly 70% of academic economists polled by the Financial Times and the University of Chicago foresee a contraction in gross domestic product next year, according to survey released June 13.

- Fed policy makers’ projections released after the meeting show the economy continuing to grow this year and next, though at a subpar pace. But they also foresee unemployment rising, something that usually only happens during a recession: Joblessness is forecast to rise to 4.1% at the end of 2024 from 3.6% now, according to the median forecast.

- While maintaining that a 4.1% jobless rate would still be historically low, Powell made clear that the Fed’s No. 1 goal was not tending to the labor market but getting inflation under wraps.

- “I will begin with one overarching message,” the Fed chair said at the start of his press conference. “We’re strongly committed to bringing inflation back down, and we’re moving expeditiously to do so.”

- To that end, policy makers are projecting a steep rise in interest rates in coming months. They now see the federal funds rate they control rising to 3.4% by the end of this year and 3.8% at the end of 2023. That’s well above the 2.5% rate they reckon is neutral for the economy — neither spurring nor restricting growth — and compares with the current fund’s rate target of 1.5% to 1.75%.