Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were $3.7 billion and year to date flows stand at -$59.9 billion. New issuance for the week was nil and year to date issuance is at $92.0 billion.

(Bloomberg) High Yield Market Highlights

- U.S. junk bonds are headed for their biggest weekly gain in more than three months after a four-session rally as investors flooded the market with cash looking for new paper. A gauge of the debt rose 0.57% Thursday, the biggest one-day gain in more than three weeks. It was headed for the best week since June, up 1.93% so far this week. The rally was partly fueled by investors returning to the asset class as US high-yield funds reported a cash influx of $3.7b for the week.

- The cash haul came at a time when the junk bond primary market faced an acute shortage of new supply, helping to bolster secondary-market prices.

- October supply is down by more than 85% from 2021; The year-to-date supply is the lowest since 2008 at $92b, versus more than $415b for the same period last year.

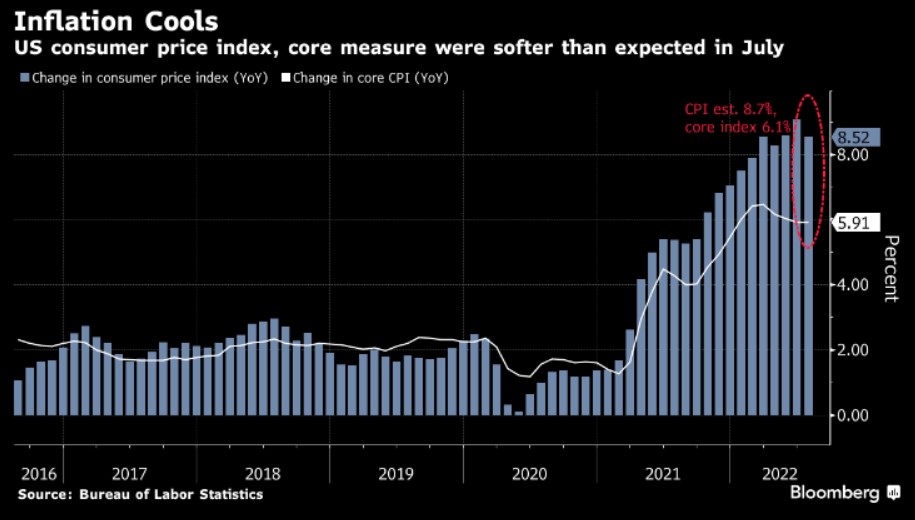

- The recent rally in junk bonds suggests the high-yield market is slowly coming around to the view that inflation’s pace is slowing and may begin to decline in the middle 2023.

- Despite continued near-term pressure, Morgan Stanley expects a “significant deceleration in the inflation path” to take hold by mid-2023, Srikanth Sankaran wrote on Monday.

- A potential window of respite from rates volatility and a more dispersed period of earnings risk should help to provide tactical support for credit markets, Sankaran wrote.

- Amid this issuance-starved market, a group of banks led by Citigroup may sell as soon as next month part of a leveraged loan that’s financing Apollo’s buyout of Tenneco, according to people with knowledge of the matter.

- The rally extended across all high yield ratings. Yields tumbled to a five-week low of 9.12% after falling for five sessions in a row, the longest declining streak in almost three months. Yields fell 56bps in the last four sessions.

- Single B and BB rated bond yields also fell to a five-week low of 9.35% and 7.33%, respectively.

- CCCs, the riskiest of junk bonds are up 1.52% this week as of Thursday, set for the biggest weekly advance in almost three months. CCC yields dropped 38bps this week to close at 15.44%, a more than two-week low.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.