Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were $0.02 billion and year to date flows stand at $0.8 billion. New issuance for the week was $7.0 billion and year to date issuance is at $27.5 billion.

(Bloomberg) High Yield Market Highlights

- US junk bonds are headed toward their biggest weekly loss in more than three months following losses for five sessions in a row, the longest losing streak since August. The week-to-date losses are at 1.01%, the most since November 4th. Yields jumped 26bps week-to-date to 8.14% after rising for five straight sessions, the longest rising streak since December. The losses extended across ratings snapping the two-week gains and ending the strongest start to a year since 2019. The sudden reversal after gaining four of the last six weeks this year came after payrolls data last Friday showed a strong jobs market, quashing hopes of the Federal Reserve pausing interest-rate hikes.

- The losses accelerated this week as a series of Fed officials reiterated their concerns about steady and stubborn inflation and the economic trajectory.

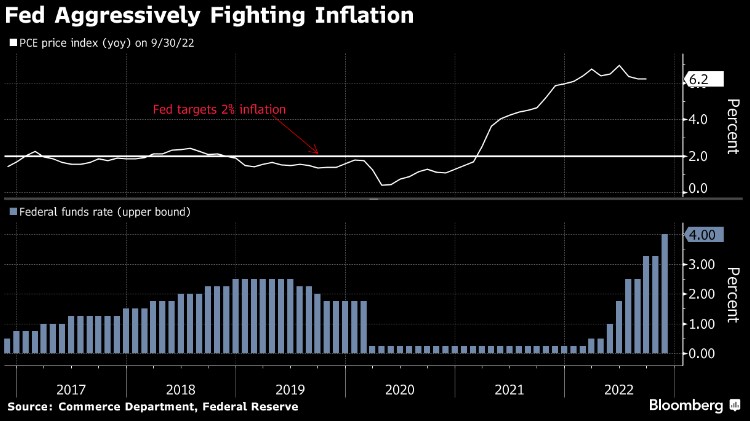

- “We need to attain a sufficiently restrictive stance of policy,” New York Fed President John Williams told a Wall Street Journal live event in New York.

- Minneapolis Fed President Neel Kashkari, an FOMC voter this year, echoed similar views at the Boston Economic Club saying rates need to be higher to combat wage growth.

- Better-than- expected macro data have called into question the “peak rates” narrative, which has been a key driver of the risk asset rally, Barclays’ Bradley Rogoff and Dominique Toublan wrote on Friday.

- Aside from Fed officials implying policy could become even more restrictive, the Fed’s Senior Loan Officer Opinion Survey (SLOOS) revealed a further tightening in bank lending conditions, and similar levels in the past have corresponded to higher forward default rates, Rogoff wrote in note.

- Even as concerns about inflation, slowing growth and Fed’s restrictive stance emerged, the primary market was open for business.

- 90% of the borrowers were just refinancing debt maturing this year or next. There was no aggressive use of proceeds such as dividend payment or funding LBOs.

- CCC yields jumped 31bps week-to-date to 12.64%, the first weekly increase this year, after rising for five consecutive sessions, the longest rising stretch since early November. CCC yields will end the five-week declining streak.

- CCCs are on track to end the week with losses. The week-to-date loss is as 0.66%.

- BB yields rose to a five-week high of 6.71% after advancing for five days in a row, the longest rising streak since September.

(Bloomberg) Powell Says Further Rate Hikes Needed and Bonds Take Heed

- Federal Reserve Chair Jerome Powell stuck to his message that interest rates need to keep rising to quash inflation and this time, the bond market listened.

- In particular, Powell floated the idea during an event in Washington on Tuesday that borrowing costs may reach a higher peak than traders and policymakers anticipate.

- The talk was Powell’s first since last Wednesday, following the Fed’s decision to raise rates by a quarter point, when markets shook off his warning that rates were headed up and rallied anyway. The chair offered similar words again but, in the aftermath of a red-hot January employment report, they hit home harder.

- “We think we are going to need to do further rate increases,” Powell told David Rubenstein during a question-and-answer session at the Economic Club of Washington. “The labor market is extraordinarily strong.”

- If the job situation remains very hot, “it may well be the case that we have to do more,” he said.

- Much stronger than expected US government data on Friday showed employers added 517,000 new workers in January while unemployment fell to 3.4%, the lowest rate since 1969. Powell said the report “shows you why we think this will be a process that takes a significant period of time.”

- Bonds sold off after an initial rally as the Fed chair opened the door to a higher peak rate in 2023 if the job market doesn’t start cooling.

- His remarks suggest that the 5.1% interest-rate peak forecast by officials in December, according to their median projection, is a soft ceiling. Powell sounded willing to follow the data and move higher if necessary.

- The Federal Open Market Committee lifted its benchmark rate by a quarter percentage point to a range of 4.5% to 4.75% last week. The smaller move followed a half-point increase in December and four jumbo-sized 75 basis-point hikes prior to that.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.