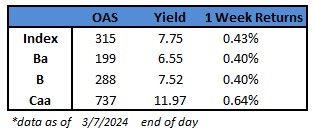

The US junk bond market is headed toward a third-straight weekly gain, with its current six-day winning streak the longest this year and yields dropping to 7.75%.

It’s allowed yields for the riskiest part of the market, CCCs, to fall below 12% for the first time this year.

They’ve fallen 21 basis points so far this week, on top of last week’s 31bp plunge, putting weekly returns at 0.64%.

CCC notes have had positive returns for 11 consecutive sessions, the longest since June, as it’s the best-performing asset class in US fixed income.

Spreads have dropped 15 basis points this week to 737, the tightest since May 2022.

The junk market’s rally gained momentum after Fed Chair Powell told Congress that rate cuts are likely this year and recession risks are not elevated in the near term.

Jobs data remains robust on the openings and unemployment claims front, ahead of this morning’s employment report for February.

Steady yields and historically tight spreads across ratings continue to draw borrowers and investors into the market.

Bloomberg Intelligence analysts Noel Hebert and Sam Geier predicted high-yield bond sales this month will range from 25b-$29b.

While things may slow some ahead of the next Fed meeting, bankers are prepping to begin a debt sale for the leveraged buyout of Truist Financial’s insurance brokerage business as loans for the deal get done.

Conversations with investors continue to indicate that yields of 7.8% in high yield and 5.3% in investment grade are attractive enough even though spreads are tight to support strong demand, Barclays’ Brad Rogoff and Dominique Toublan wrote in note this morning.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.

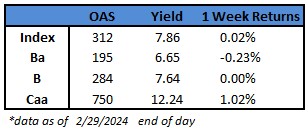

The broad rally in risk assets has propelled CCCs, the riskiest part of the junk bond market, to the top as the best performing asset class in February. Returns for the month were 1.7% after climbing for six consecutive sessions. The gains came after S&P 500 breached the 5,000 level and steadily climbed to close at an all-time high.

CCC returns turned positive year-to-date for the first time in the last week of February, only to accelerate to rise as the best asset class for total returns in the US fixed income market.

CCC yields tumbled 43 basis points in February to close at a nine-week low of 12.24% bucking the broader trend as BB yields rose 17 basis points to 6.65%. Single B yields barely moved to close at 7.64%.

Broad macro economic data reiterated the narrative about strong and resilient growth amid a slower-than-expected decline in inflation. However, robust economic growth, against the backdrop of relatively stable inflation reading, bolstered risk assets across markets.

The recent outperformance of lower-quality assets has coincided with large gains in some of the riskier and more speculative parts of the market, such as cryptocurrencies, Barclays analysts Brad Rogoff and Dominique Toublan wrote in a Friday note.

Loose financial conditions continue to support risk-taking in the markets, they wrote.

Though spreads are historically tight, yields are supporting strong demand, the analysts reiterated again this morning.

Tight spreads, attractive yields and resilient economy have drawn US borrowers into the market powering a supply boom.

February supply of almost $27b pushed the year-to-date tally to $58b, a 70% jump year-over year.

New bond sales in February were up 86% over last February.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.

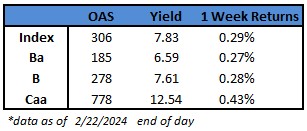

US junk bonds notched their biggest one-day gains in more than four weeks and are poised for a rebound off last week’s losses to score the biggest weekly gains in four, as equities hit an all-time high, driving spreads to a more than two-year low of 306 basis points.

With the Federal Reserve signaling caution about its next move, credit markets remain quite “upbeat,” with strong “yield-driven” demand, Barclays analysts Brad Rogoff and Dominique Toublan wrote this morning.

While inflation risks remain in focus, growth is resilient and corporate earnings are still strong across cyclicals and noncyclicals, they wrote, adding that higher yields continue to compress spreads.

Dollar prices in the junk bond market are still low, making yields attractive to investors and supporting strong demand.

Spreads were crushed across ratings, with BB spreads tumbling to 185 basis points, the lowest since Jan. 2020.

Single B spreads plummeted to 278 basis points, the lowest since July 2007.

CCCs spreads dropped to a more than eight week low of 778 basis points, the lowest since December.

The gains were across the board as risk assets shrugged off inflation concerns and rallied on a resilient economy and strong labor market.

Yields dropped seven basis points to 7.83% and spreads moved closer to 300 basis points.

US borrowers are capitalizing on demand supported by low spreads and higher yields.

The primary market has priced more than $4b in new bonds this week, putting issuance at $23b for the month.

Year-to-date supply is at $54b, up 59% year-over-year.

Robust corporate earnings, combined with strong macro data, have pushed back recession concerns and bolstered risk assets.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.

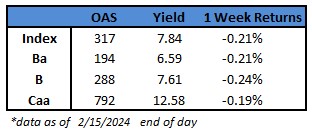

US junk bonds may end a three-week rally as they head to close the week with modest negative returns. Markets were jolted earlier this week when faster-than-expected inflation caused the biggest one-day loss in four months.

The consumer price index rose by more than forecast in January on a monthly and annual basis, suggesting that the road back to the 2% inflation target will be bumpy.

However, the markets quickly pared those losses. The rebound got a boost after data showed US factory production declined for the first time in three months and retail sales dropped in January, indicating that inflation will moderate steadily toward the target.

Yields climbed to a five-week high of 7.91% on Tuesday after the surprise rise in inflation, but dropped to 7.84% after data showed retail sales fell the most in year and factory production declined. However, yields are still up nine basis points week-to-date at 7.84%.

The modest losses extend across ratings in the US junk bond market. CCC yields rose eight basis points for the week to 12.58% after jumping to 12.68% on Tuesday.

BB yields closed at 6.59% after rising to 6.63%, up eight basis points for the week. BBs are headed toward a second straight week of losses.

As the market was rattled by inflation data, US borrowers stayed on the sidelines as they assessed the risk appetite.

The primary market was relatively quiet after Monday. More than $6b priced on Monday to make it the busiest day since April 2023.

The month-to-date supply stood at almost $19b and year-to-date at $50b.

Even amid volatility, spreads were closer to 300 basis points and yields were still below 8%.

Barclays expects spreads to compress further to a range of 290-315 basis points in the next six months.

Marginal demand for yield is strong, and spreads seems to be an afterthought, Brad Rogoff and Dominique Toublan of Barclays wrote this morning.

We see limited headwinds from the macro side and credit fundamentals, they wrote.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.

After a bumpy start to the year, US junk bonds are headed for their third straight week of gains, propelled by CCCs, the riskiest tier of the high yield market.

Gains spanned across the market, spurred by economic growth backed by strong labor market, expanding business activity and cooling inflation data, brushing off Federal Reserve officials’ chorus reiterating that the central bank is not in a hurry to ease monetary policy.

Risk assets were mostly higher this week, along with yields, as earnings results remained largely positive, Barclays’ Brad Rogoff and Dominique Toublan wrote on Friday

With macro data still benign, spreads should continue to react to yield moves as the incremental buyer is yield-focused, they wrote

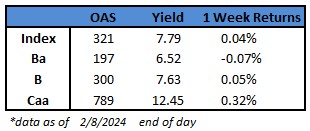

CCC yields fell 11 basis points week-to-date to 12.45%, the biggest weekly decline within the high yield market. CCCs are on track to be the best performing asset in the US junk bond market, with week-to-date gains of 0.32%

The rally gained legs as fears of a recession receded in the backdrop of continuing strength in the labor market as US unemployment claims fell for the first time in three weeks

The broader US high yield index yield rose by three basis points to 7.79%. The rally in CCCs drove the modest gains in broader index

As spreads dropped to a six-week low of 321 basis points and yields hovered near 8%, US borrowers continued to crowd the primary market. Borrowers were in a hurry to capitalize on the still-low cost of debt, yet high enough to attract buyers, before the economy begins to show some expected signs of slowing in the second half

After a busy January, with the month-to-date supply at $8.55b, February is on track to be the busiest since 2021

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.

US junk bond supply so far this month is 13% above that for all of January 2023, helped by $3.5b of sales Thursday that was the busiest session in three months.

The market is on track to have its heaviest overall month in more than two years, with new borrowers led by sponsor-owned companies rushing to refinance debt and extend maturities. Yields have held firmly below 8% and spreads remain below 350 basis points.

At least four borrowers are expected to sell about $4b in the coming days

Economic data continue to bolster sentiment, the latest being GDP growth trouncing forecasts amid a jump in personal spending

Resilient growth, strong business investment and new home sales have spurned recession calls and bolstered risk assets

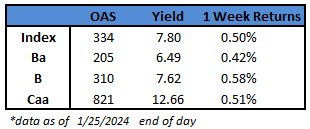

Junk bonds are headed for weekly gains, with yields down 9bps to 7.80% and spreads narrowing 4bps to 334bps

Strength has been across ratings

BB yields have dropped back below 6.5% and spreads hover near 200bps, with the segment returning 0.4% so far this week

CCCs have climbed for six consecutive sessions, generating combined gains of 0.5% since Monday

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.

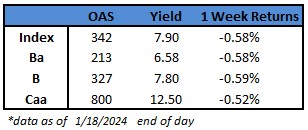

A back-and-forth start to the year has continued this week for the US junk bond market, which rose last week after starting 2024 with a loss.

Yields have climbed 19 basis points since last Friday to 7.90%, following a week of robust economic data on retail sales, housing sentiment, industrial production and unemployment claims. The readings renewed concerns that the Federal Reserve may delay easing interest-rate policy, with investors paring rate-cut bets and Treasury yields climbing.

High-yield’s losses gained legs as Fed Governor Christopher Waller’s comments Tuesday signaled the central bank isn’t in a hurry to cut rates

Atlanta Fed President Raphael Bostic joined the chorus Thursday, urging policymakers to proceed cautiously toward rate cuts

At the same time, strong data supported the soft landing narration and bolstered views that a recession is unlikely

US borrowers crowded the primary market during this holiday-shortened week as yields are still below 8% and spreads are under 350 basis points

More than $5.5b of deals were priced, putting January’s total above $12b and at 60% of volume in the opening month of 2023

Junk bond yields climbed across ratings. BB yields jumped 18 basis points week-to-date to 6.58%

(Bloomberg) Waller Urges Cutting Rates ‘Carefully’ If Inflation Cools

Federal Reserve Governor Christopher Waller said the US central bank should take a cautious and systematic approach when it begins cutting interest rates, a process that can start this year absent a rebound in inflation.

“As long as inflation doesn’t rebound and stay elevated, I believe the FOMC will be able to lower the target range for the federal funds rate this year,” Waller said at a virtual event hosted by the Brookings Institution on Tuesday.

“When the time is right to begin lowering rates, I believe it can and should be lowered methodically and carefully,” he added.

The Fed governor offered some of the most detailed remarks to date around the Fed’s intentions to ease policy this year. While Waller showed an openness to cutting rates, his comments also appeared to push back against market expectations for as many as six rate cuts this year.

“With economic activity and labor markets in good shape and inflation coming down gradually to 2%, I see no reason to move as quickly or cut as rapidly as in the past,” he said, pointing to previous economic shocks that have precipitated rapid rate cuts.

Treasury yields jumped in the wake of Waller’s comments. Traders pared back the probability of a rate cut as soon as March as well as the degree of total policy rate declines seen for the full year.

He said the timing of cuts and the actual number “will depend on the incoming data.”

Waller’s remarks highlighted his intention to balance risks to both sides of the Fed’s mandate and avoid staying restrictive for too long, while also not beginning to reduce rates before their 2% inflation goal was secure. He noted that he needs to see a moderation in consumption and hiring as well as continued low readings on monthly inflation data to bolster the case for a cut.

While Waller said he’s becoming more confident that policymakers are “within striking distance” of reaching their 2% inflation target, “I will need more information in the coming months confirming or (conceivably) challenging the notion that inflation is moving down sustainably toward our inflation goal.”

If policymakers see a continuation in the trends seen in the real data and inflation data, “we can slowly calibrate the real rate cut down,” he said. “If we think we need to move it faster, we can move it faster depending on what the data says. But the key is we have the flexibility that we can be methodical and careful.”

He added that once the Fed is relatively convinced that inflation is sustainably near the central bank’s 2% target, policymakers can “start thinking how fast we want to cut, or how long, what the pace is, or how big.”

As for the central bank’s balance sheet, Waller said it would be reasonable to start thinking about slowing the pace of asset runoff “some time this year.”

While Waller’s language suggested he favors starting rate cuts sooner rather than later, his comments also weren’t “a ringing endorsement” for a March cut, Bank of America’s Michael Gapen wrote. Instead, he said, the key takeaway of Waller’s speech related to the pace of easing.

Economists at Goldman Sachs also noted that Waller’s remarks “raise the risk that the first cut could come slightly later than our forecast of March and that the pace of cuts could be quarterly from the outset.”

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.

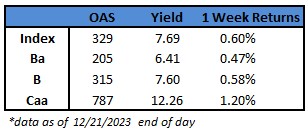

The fourth quarter US junk bond rally spurred by the Federal Reserve drove yields further down to a new 16-month low of 7.69% and spreads to a another 20-month low of 329 basis points accelerating gains in CCCs, the riskiest tier of the junk bond market.

CCC yields tumbled to a 10-month low of 12.26% and spreads closed at a 19-month low of 787 basis points.

CCCs amassed gains of almost 19%, the best year since 2016. The fourth quarter returns so far stand at 5.95%, on track to be the biggest quarterly gains since December 2020.

CCCs are the best asset class in the US fixed income market as they outperform single Bs, BBs and investment grade.

Bloomberg Economics expects that the Fed will lead the way with 125 basis points of cuts over the course of 2024, Tom Orlik wrote on Tuesday.

After the Fed’s own quarterly projections indicated that the central bank will lower interest rates by 75 basis points next year, yields and spreads dropped across all ratings in the US high yield market.

BB yields dropped to a new 10-month low of 6.41%. Yields have fallen 158 basis points since the November Fed meeting and 59 basis points so far this month. Spreads were at 205 basis points, down 90 basis points year-to-date after falling 120 basis points so far this quarter.

The rally drew both borrowers and investors into the market, spurring new bond sales.

The primary market is expected to be largely quiet ahead of the holidays.

Forecasts for junk-bond supply in 2024 generally range from around $200 billion to $230 billion.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.

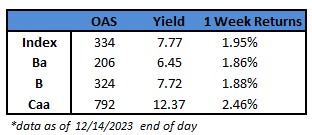

US junk-bond yields plunged to a 10-month low and spreads dropped to a 20-month low after the Federal Reserve paused the most aggressive policy of raising interest rates for the third time in this week’s meeting, while also forecasting a series of rate cuts next year. Yields closed at 7.77% and spreads at 334 basis points. Junk bonds are headed for the fifth straight week of gains, with 1.95% returns week-to-date.

The broad rally in high-yield bonds on news of the Fed pivoting to rate cuts spurred CCCs — the riskiest of junk debt — to post the biggest one-day gains in three years, with returns of 1.6% on Thursday. CCC yields tumbled 67 basis points to 12.37%, also a 10-month low. The demand for yield is not abating, Brad Rogoff and Dominique Toublan of Barclays wrote Friday morning.

The rally in junk bonds, powered by a resilient economy and easing financial conditions, got further impetus from the Fed’s summary of economic projections. The central bank revised the growth forecast for 2023 to 2.6% from 2.1% it estimated in the September report.

The Fed’s own quarterly projections showed it expects to lower rates by 75 basis points next year, a sharper pace of cuts than indicated in September.

Bloomberg Economics expects rate cuts as early as March of next year.

Gains in the US high-yield market were seen across ratings. Strong demand for credit to continue in the near-term, helping spreads grind tighter, Rogoff and Toublan wrote.

The broader high-yield index racked up returns of 1.24% at close on Thursday.

BB yields dropped 28 basis points to a 10-month low of 6.45% and spreads closed near a two-year low of 206 basis points.

Single B yields fell 32 basis points to 7.72%, a 16-month low.

Strong risk appetite, falling yields and spreads, and steady economic growth brought US borrowers into the market, driving new bond sales to $12b so far this month, already more than five times that of Dec. 2022.

Issuance was predominantly for refinancing bonds and term loans.

Most new sales priced at the lower end of price talk and drew orders of about three times the size of the offering.

US junk bonds are poised to extend the rally on a broad risk-on sentiment after Chair Jerome Powell reinforced market expectations of a pivot to rate cuts.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.

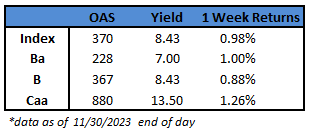

The broad November rally in risk assets propelled CCCs, the riskiest tier of the junk bond market, alongside equities, to post the biggest monthly returns since January of this year. CCC yields plunged 125 basis points in November, also the most in 10 months, to 13.50%, driving gains of 4.53%.

The broad surge across risk assets was fueled by a market consensus that the Federal Reserve was finished with the most aggressive tightening cycle in decades and that it will begin to ease monetary policy by the middle of 2024. Junk bond spreads dropped to a 10-week low of 370 basis points, after falling 67 basis points in November, the biggest monthly decline in five months.

The rally came as the 5- and 10-year Treasury yields dropped by about 60 basis points each during the month of November to close at 4.27% and 4.33%, respectively. Treasury yields plunged from near 5% on Oct. 19

US junk bonds racked up gains of 4.53%, the largest in a month since July 2022, fueled by BBs. Yields fell 106 basis points to 8.43%, also the biggest monthly decline in 16 months

BBs had the best performance in 16 months, with returns of 4.6% reversing the three-month losing streak as rates tumbled

Yields crashed by 99 basis points to close near a four-month low of 7%, the biggest monthly decline in over a year

Resilient growth, cooling inflation and a softening labor market gave a strong impetus to the November rally, luring investors and US borrowers from the sidelines

November is the fourth busiest month for issuance as volume surged to $19.4 billion, more than double October’s total of $9.45 billion

US junk bond funds were inundated with new cash as investors poured more than $11b in November

Year-to-date supply stood at $163 billion, up by about 60% from 2022’s $102 billion

Forecasts for junk bond supply in 2024 range from $200 billion to $230 billion, with the exception of BofA, which estimates gross supply to be around $165 billion, a 5% drop from its projection of $175 billion for 2023

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.