Fund Flows & Issuance: According to a Wells Fargo report, flows week to date were -$0.1 billion and year to date flows stand at $12.6 billion. New issuance for the week was $0.0 billion and year to date HY is at $165.0 billion, which is +26% over the same period last year.

(Bloomberg) High Yield Market Highlights

- U.S. junk bonds have recouped this month’s losses and look set to extend higher as stock futures rise ahead of Chair Jay Powell’s Jackson Hole speech.

- Funds have reported net inflows of $10.4b YTD vs outflows of more than $20b for the same period last year

- Month to date, the high-yield index is flat, following a 0.15% gain yesterday

- Junk bonds gained across the risk spectrum for five straight sessions, with CCCs gaining 0.17%, the most in high yield yesterday, compared to 0.15% for BBs and single-Bs respectively

- The energy index led the CCC rally, posting gains for five consecutive sessions for the first time in more than eight weeks, with a YTD return of 3.21% after a gain of 0.4% yesterday

- Junk bond yields dropped for five straight sessions to close at a fresh 2-month low of 5.78%

- Spreads were steady, tightening around 3-4bps across ratings and moving in tandem with the 5Y UST yields which were up 3bps

- Junk bond return YTD is 10.55%, close to the 2019 peak of 10.57%

- BB returns hit a new 2019 peak at 11.92% after posting returns of 0.15%

- Single-Bs, second best in high yield, were 10.74%, just 2bps off the YTD peak of 10.76%, after gaining 0.15% yesterday

- CCC YTD returns were 5.47% after 0.17% returns yesterday

- Summer lull descended on the primary

- August priced $9.65b over 11 deals, the slowest month of this year

- Supply is expected to resume after Labor Day

(Bloomberg) CyrusOne Explores a Sale After Bidder Approach

- CyrusOne Inc. is considering a potential sale after receiving takeover interest, according to people familiar with the matter, as digital infrastructure companies such as data center operators increasingly garner buyout interest from rivals and private buyers.

- The Dallas-based company is working with an adviser to evaluate strategic options after a recent approach from at least one potential suitor, said the people, who asked to not be identified because the matter isn’t public.

- A bidder group including KKR & Co., Stonepeak Infrastructure Partners and I Squared Capital is in the preliminary stages of weighing a bid for the company, said one of the people. Other potential bidders are interested too, the people said. No decision has been made and CyrusOne could opt to remain independent, they said.

- CyrusOne rose as high as 16.6% on the news, its biggest gain since going public in 2013. The shares were up 11.7% to $72.79 at 11:36 a.m. in New York on Friday, giving the company a market value of about $8.2 billion.

- A representative for KKR declined to comment. Representatives for Stonepeak, I Squared and CyrusOne didn’t respond to requests for comment.

- Founded in 2001, CyrusOne has a network of 48 data centers serving about 1,000 customers in the U.S., U.K., Singapore and Germany, according to its annual report. It is one of at least five real estate investment trusts that specialize in data centers, which help companies safely store data. Others include Equinix Inc. and Digital Realty Trust Inc.

(Bloomberg) Junk-Debt Market’s Flight to Quality Is About to Heat Up Again

- Companies selling debt in the U.S. leveraged loan and junk bond markets after Labor Day may find investors have a stronger appetite for quality than risk.

- The deal pipeline for both types of debt indicates higher rated, well-known companies plan to seek financing in the coming months. They are likely to be well-received by investors worried about a recession yet still looking for yield.

- “Investors are likely to remain highly selective but will be buyers in size for the structures that compare favorably to paper available in the secondary market,” said Jeff Cohen, Credit Suisse’s global head of leveraged finance capital markets.

- Amid negative sentiment due to the trade war and a possible global recession, riskier loan sales have struggled in the $1.2 trillion market. The loan market has seen five borrowings scrapped in recent weeks: Vewd Software USA LLC, Golden Hippo, Glass Mountain Pipeline Holdings LLC, Life Time Inc. and Chief Power Finance LLC.

- High-yield bore the brunt of this month’s sell-off, but has since clawed backsome of those losses.

- The high-yield market hasn’t seen a deal price since Aug. 12, yet about $20 billion of issuance may come in September, Bank of America Corp.’s Oleg Melentyev said. That compares to $23 billion in September 2018, and $40 billion in both 2016 and 2017. The market is about $1.24 trillion in size.

(Bloomberg) Cracks Forming in Leveraged Loan Market as Another Deal Pulled

- The froth may not be off leveraged loans just yet, but with five deals falling through in the past few weeks, the market is definitely a little less giddy.

- This time it’s Vewd Software. The streaming-service provider joins marketing firm Golden Hippo, Glass Mountain Pipeline Holdings LLC, Chief Power Finance LLC and fitness-center builder Life Time Inc. in dipping its toe in the water and finding borrowing conditions too cold.

- The leveraged loan market has been a favorite of private equity firms, funding payouts to partners and buyouts of targeted companies at record-low borrowing costs for a decade, doubling in size to about $1.2 trillion. Now it’s experiencing a rare moment of sobriety. Investors who smell a recession are shying away from companies that just a few months ago might have been an easier sell.

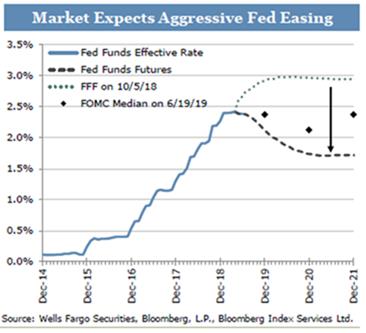

- It’s not just failed offerings that are flashing yellow caution lights. Some borrowers have come to market and had to pay more than they originally planned. The possibility of continued rate cuts by the Federal Reserve has made floating-rate deals less attractive, and companies vulnerable to trade wars have had to promise higher yields.

- The market has seen “widely divergent pricing outcomes,” said Jeff Cohen, global head of leveraged finance capital markets at Credit Suisse Group AG.

- DNA-testing firm Ancestry.com Inc., for example, increased the pricing of a loan financing a dividend to its private equity owners and reduced the size of the payout by $200 million.