CAM Investment Grade Weekly Insights

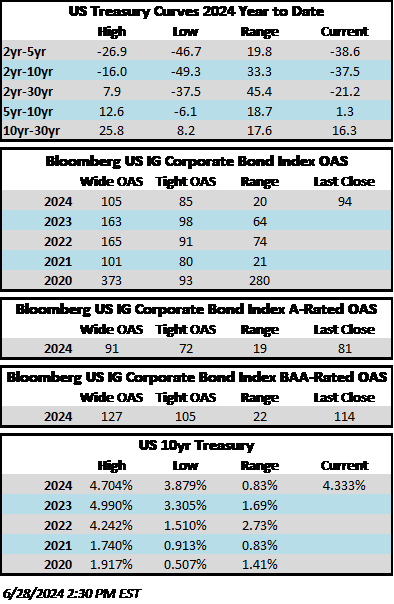

Credit spreads were little changed during the week. The Bloomberg US Corporate Bond Index closed at 94 on Thursday June 27 after closing the week prior at the same level. The 10yr Treasury yield is slightly higher on the week, trading at 4.33% this Friday afternoon after closing last week at 4.26%. Through Thursday, the corporate bond index YTD total return was -0.02% while the yield-to-maturity for the benchmark was 5.43%.

Economics

Economic data this week was mostly in line with consensus and there were no major surprises. Highlights included a consumer confidence reading that was slightly below expectations and personal income data that came in slightly above expectations. The biggest release this week was Friday morning’s PCE price index which was about as consistent with expectations as it possibly could be. The release showed that the disinflationary environment sustained some momentum during May but it was probably not enough to make the Fed turn dovish. Continued progress will be needed if the Fed expects to follow through with two cuts in the latter half of the year. Next week is another disjointed one with several important releases early in the week (PMI, ISM manufacturing/services and durable goods) followed by a market holiday on Thursday in observance of Independence Day. The biggest release of the week occurs on Friday morning with the employment report for the month of June. Looking ahead, the Fed does not meet again until the very end of July.

Issuance

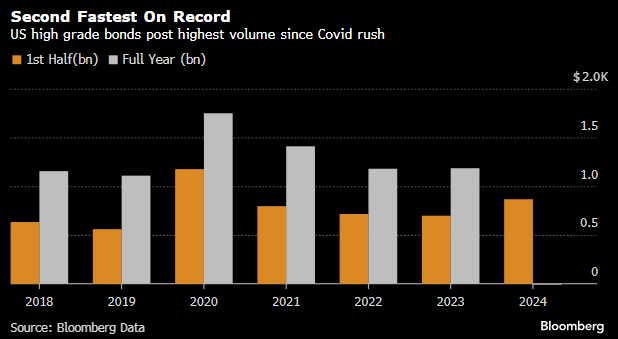

The IG primary market was strong this week as borrowers priced nearly $32bln in new debt, well ahead of the $20bln estimate. More than half of this week’s volume was from borrowers outside the U.S., with Asia Pacific firms and governments leading the way. So, although issuance was robust, it wasn’t coming from borrowers that are necessarily household names. Next week syndicate desks are looking for a quiet week with just $5bln of issuance and only $80bln of issuance for the seasonally slow month of July (that estimate would make it the lowest volume month so far in 2024). According to sources compiled by Bloomberg, after a record first quarter, the pace of issuance in 2024 slowed during the second quarter making 2024 the second busiest first half to a year on record. It was eclipsed only by the surge in borrowing that occurred during the trading days that followed the official onset of the 2020 pandemic.

Flows

According to LSEG Lipper, for the week ended June 26, investment-grade bond funds reported a net inflow of +$0.389bln. Short and intermediate investment-grade bond funds have seen positive flows 23 of the past 26 weeks. YTD flows into IG stand at +$37.2bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.