CAM High Yield Weekly Insights

(Bloomberg) High Yield Market Highlights

- US junk bonds are headed for a third straight week of gains as investors continued to bet that the Federal Reserve will cut rates more than once this year, with retail sales data this week showing signs of consumer strain. Adding more evidence that the economy continued to slowdown, data for continuing claims, a proxy for the number of people receiving unemployment benefits, rose for a seventh straight week to 1.82m, just 1,000 shy of the highest level since the end of 2021, indicating the labor market is also cooling.

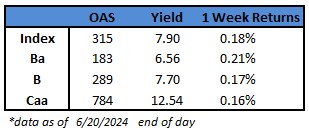

- Yields were range-bound this holiday-shortened week and are poised to decline modestly for the third consecutive week. Yields closed at 7.90% on Thursday.

- The primary market has seen a steady stream of borrowers this week. Six companies sold a little more than $3b in just three sessions

- The month-to-date volume is $14b

- The modest gains in the US junk bond market cut across all ratings, though CCC yields were set to climb for the fifth week in a row, closing at 12.54% on Thursday, the longest rising streak in more than two years

- CCCs, however, scored gains of 0.04% on Thursday, and are likely to close the week with modest gains. The week-to-date gain stand at 0.16%

- BBs are also on track for fourth week of positive returns, with week-to-date gains at 0.21%. BB yields fell five basis points week-to-date to 6.56%, also largely range bound, and may decline for the third week in a row

- US high-yield debt issuers delivered a solid first quarter with elevated earnings and generally positive guidance, JPMorgan strategists led by Nelson Jantzen wrote in note last week

- Even while credit metrics showed some modest erosion, leverage remains comfortably below the long-term average, Jantzen wrote

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.