CAM Investment Grade Weekly Insights

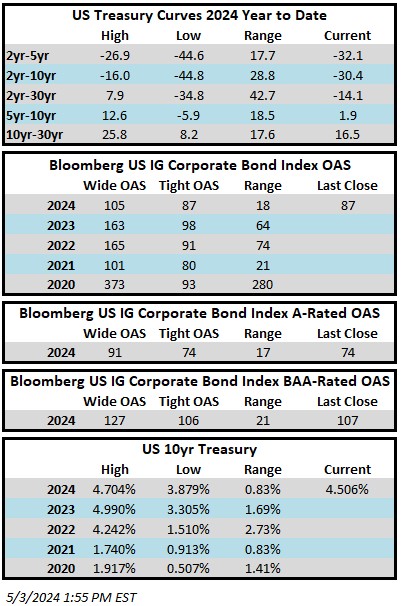

Credit spreads stuck to a tight range during the week and are looking as though they will finish the period relatively unchanged from where they began. The Bloomberg US Corporate Bond Index closed at 87 on Thursday May 2 after closing the week prior at the same level. The 10yr Treasury yield is lower this week, trading at 4.51% this Friday afternoon after closing last week at 4.66%. Through Thursday, the corporate bond index YTD total return was -2.20% while the yield-to-maturity for the benchmark was 5.60% relative to its 5-year average of 3.67%.

Economics

It was a busy week for data with the two main events being the FOMC on Wednesday and the April payroll report on Friday. The Fed release was in-line with expectations although Chairman Powell was clear that the committee does not anticipate additional rate hikes. The prospect for additional hikes was a theme that some investors had been latching onto in recent weeks so it was reassuring for the dovish camp to hear Powell address this specifically. The Fed then got the type of data point they have been looking for with Friday’s jobs report: average hourly earnings came in cooler than expectations and job gains for April slowed to 175,000 versus the survey estimate of 240,000. This was the lightest monthly print for payrolls since October of last year. Next week is an extremely light week for economic data with the only meaningful prints in the latter half of the week with jobless claims and consumer confidence releases.

Issuance

It was a reasonably busy week for issuance considering the backdrop of earnings and the FOMC meeting as IG-rated companies printed $19bln of new debt. Syndicate desks are looking for a busier week next week with an estimate of $30bln. The window for new issuance will start to open up as earnings season winds down and with the lack of the aforementioned “market-moving” economic releases. Year-to-date issuance stands at $636bln.

Flows

According to LSEG Lipper, for the week ended May 1, investment-grade bond funds reported a net inflow of +$812mm. IG funds have seen positive flows 17 of the past 18 weeks. YTD flows into IG stand at +$33.7bln.

This information is intended solely to report on investment strategies identified by Cincinnati Asset Management. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. This material is not intended as an offer or solicitation to buy, hold or sell any financial instrument. Fixed income securities may be sensitive to prevailing interest rates. When rates rise the value generally declines. Past performance is not a guarantee of future results.