CAM Investment Grade Weekly Insights

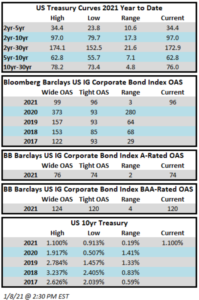

Spreads will finish the week unchanged after a minor bout of mid-week volatility that pushed spreads wider for a day. Through the Thursday close, the OAS on the Bloomberg Barclays Corporate Index was 96, which is the same level that it closed to end 2020. Treasury rates stole the headlines from spreads this week and are higher across the board, with the 10yr up 19 basis points week over week. The sell-off in Treasuries began ahead of the Georgia special election and accelerated after the results, as the market began to price the expectation of more stimulus and Treasury supply. Interestingly, rates were even able to shrug off a woeful December jobs report that showed the loss of -140k jobs during the month versus the concensus estimate for an addition of +50k. We remain concerned about the health of the labor market, elevated unemployment and its impact on the economy’s ability to grow.

The high grade primary market was back in business this week with a strong start to the year as issuers borrowed $50bln. It will be interesting to monitor new issue supply as 2021 progresses. There are expectations for less supply but will this hold true? In our view it is really a question of the economy and how quickly things get back to “normal.” If things go swimmingly, then we would expect less supply but if re-opening takes longer than expected then that would be a case for more supply as companies that are more impacted by the pandemic may need to continue to tap the new issue market for balance sheet liquidity.

According to data compiled by Wells Fargo, inflows into investment grade credit for the week of December 31-January 6 were +$8.4bln.