CAM Investment Grade Weekly Insights

Fund Flows & Issuance: According to Wells Fargo, IG fund flows for the week of March 15-March 21 were a positive $167 million, though flows have slowed now for four consecutive weeks. The data analyzed by wells shows that longer duration funds are gathering flows at the expense of shorter duration funds. This is in contrast to Lipper data, where IG saw a solid inflow of $3.5bn versus the 4-wk Lipper average of +$1.6bn. HY outflows continue, with Lipper reporting an outflow of $1.17bn taking YTD outflows to nearly $18bn for the HY asset class.

The IG new issue calendar saw $26.875bn price on the week, as Anheuser-Busch InBev led the way with a $10bn print across six tranches. Corporate issuance is down 18% y/y but there are several large M&A related deals waiting in the wings that could narrow this gap substantially in the coming weeks. It is also likely that the market tone and renewed volatility in stocks and rates are keeping some issuers on the sidelines for the time being.

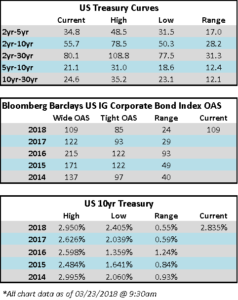

The Bloomberg Barclays US IG Corporate Bond Index opened on Friday with an OAS of 109, which is widest level yet seen in 2018.

(WSJ) ‘Rolldown’ Shows Why the Bond Market Is an Unfriendly Place to Hide

- For bond investors, a concept called “rolldown” is like a virtuous form of financial gravity, a force that generates returns without doing much work. A flattening yield curve, however, is threatening the physics that investors rely upon.

- The signals sent by the Federal Reserve Wednesday suggests the yield curve could flatten further: Its rate increases will raise short-dated yields, but there is still skepticism that rates in the long term will be materially higher.

- When the yield curve is steep, investors benefit from the yield on a long-term bond “rolling down” the curve. As a 10-year bond over time becomes a nine-year bond, all else being equal, its yield falls and its price rises, producing a gain above the initial yield when the bond is purchased. That offers protection for bond investors in a rising-rate environment, notes TwentyFour Asset Management.

- The U.S. yield curve still slopes upwards, with 10-year Treasurys yielding 0.57 percentage point more than two-year securities. But the further out you go, the flatter the curve gets. There is now only a 0.07 percentage-point gap between seven- and 10-year Treasury yields, a gap that has more than halved from a year ago. The potential for rolldown gains is small.

- A similar phenomenon is showing up in U.S. corporate bond markets too, with the gap between short- and long-maturity bonds shrinking in both yield and spread terms. A number of forces are potentially at play here, as with the rise in Libor rates.

- Higher U.S. Treasury bill issuance is competing for investors’ cash. And the pool of funding for short-dated debt may also have shrunk due to corporate cash repatriation, Citigroup suggests: if dollars can be repatriated and spent, they don’t need to be tied up in bond investments.

- By contrast, steeper curves in eurozone government and corporate bond markets may make them attractive to investors. The European Central Bank’s negative-rate policy, which it is in no rush to change, is acting as an anchor for yields, reassuring bond investors. Coupled with the cost for foreign investors to hedge dollar-denominated bonds, U.S. bonds lose out despite their higher yields. All of that may lead to tighter U.S. financial conditions.

(Bloomberg) Bayer Hopes to Close $66 Billion Deal With Monsanto in 2Q18

- Bayer continues to await antitrust clearance from the U.S. Department of Justice to close its proposed $66 billion purchase of Monsanto after having obtained all other necessary approvals. A DOJ decision is likely in 2Q. While Bayer agreed to sell or license about $7 billion worth of assets to BASF to ease antitrust concerns, additional measures may be needed for approval. Though this is more likely than not to be secured, if antitrust issues prevent it, Bayer will owe Monsanto a $2 billion fee.

- Bayer also has ongoing patent suits against generic-drug makers with respect to Xarelto (with J&J), Beyaz/Safyral, Betaferon/Betaseron, Damoctocog alfa pegol, Finacea, Nexavar and Staxyn. It’s involved in product liability litigation with respect to Yasmin, Mirenac and Xarelto. Other legal issues include environmental and tax matters.

(Bloomberg) PG&E Has a Plan to Prevent More Deadly Wildfires

- Five months after wildfires ripped through Northern California’s wine country, PG&E Corp. has developed a plan to lower the risk of another outbreak.

- PG&E will establish new guidelines for proactively turning off power lines in areas where there’s extreme fire risk — a practice that regulators had asked about after last year’s events. The company will also keep trees and limbs farther away from power lines to meet new standards and expand its practice of disabling some equipment during fire season, according to an emailed statement Thursday.

- The announcement comes as state investigators probe whether PG&E power lines played a role in causing fires in Napa and Sonoma counties that destroyed thousands of structures and killed at least 40 people. The San Francisco-based company has lost more than a third of its market value amid investor concern that its equipment may have sparked the deadly blazes. No cause has been determined.